Important facts

- What is the CBAM?

- An EU mechanism that equalizes CO₂ costs for imported goods from third countries in order to avoid distortions of competition and carbon leakage.

- When does it apply?

- The transition phase ended with the last quarterly report for Q4/2025 (deadline: 31.01.2026). Since then, the regular phase with authorization and recording has been running, followed by certificate sales from February 2027 and the first annual declaration for the import year 2026 must be submitted by September 2027.

- Which products are affected?

- Products such as cement, iron & steel, aluminium, fertilizers, hydrogen and electricity are affected by CBAM.

- Who is obliged to do this?

- Importers of affected products into the EU.

- How does it work?

- Affected importers must calculate the emissions during production and purchase and surrender CBAM certificates according to the quantity of emissions.

- What are the goals?

- Avoiding carbon leakage, promoting climate-friendly production worldwide and supporting the EU's climate targets.

Summary & Updates

The Carbon Border Adjustment Mechanism (CBAM) regulates the CO₂ emissions of imported goods and thus prevents carbon leakage. European companies should not be disadvantaged by their climate protection measures. Imports from countries with lower environmental standards are therefore subject to the same CO₂ costs. At the same time, the mechanism is intended to motivate trading partners to introduce their own CO₂ pricing systems. The revenue flows into sustainable projects to further promote climate protection.

Importers must buy CO₂ certificates based on EU emissions trading and calculate and report the CO₂ footprint of their products. Countries with comparable climate protection measures can be exempted from payments. Emission-intensive industries such as steel, cement, aluminium, fertilizers and electricity are particularly affected.

CBAM offers opportunities, for example through innovation incentives, low-emission technologies and planning security, but also brings challenges: higher costs, administrative effort and possible disadvantages for developing countries.

Companies that focus on sustainability at an early stage can strengthen their competitiveness and take on a pioneering role. CBAM could also serve as a global model and initiate climate protection measures worldwide.

The most important innovations of the CBAM amendment (February 2026)

Anyone who imports less than 50 tons of CBAM goods per year is exempt from all obligations. This applies cumulatively to aluminium, cement, fertilizers and iron & steel, but not to electricity and hydrogen.

In future, the annual declaration will only be due by September 30 instead of the previous deadline of the end of May. This provides more breathing space in the first full standard year.

The quarterly coverage obligation is reduced from 80% to 50% of the required quantity of certificates.

A check is only necessary if actual emission values are reported. If you work with default values, this step is not necessary.

The Commission can set annual standard CO₂ prices for third countries. Those who use standard emission values can only take standard CO₂ prices into account. Those who report actual values remain under the full obligation to provide evidence.

Penalties can be reduced if it can be proven that false declarations were caused by third parties. In addition, companies can be exempted from declaration and tax obligations under certain conditions by making a payment.

In future, they must act as authorized CBAM declarants and are liable for the obligations of the importers they represent.

Anyone who submits an application for approval by March 31, 2026 may continue to import until the decision is made, so supply chains remain secure.

CBAM: Definition, goals & background

Definition and basics

The Carbon Border Adjustment Mechanism (CBAM) is an instrument of the European Union. It aims to adjust imports from countries with lower climate protection standards to the European CO₂ price. It is a central component of the EU Green Deal and the European Commission's Fit for 55 package, which aim to reduce the EU's greenhouse gas emissions by 55% by 2030 compared to 1990 levels.

In order to ensure the competitiveness of European companies and achieve environmental targets, the CBAM requires importers to purchase CO₂ certificates for certain products. These certificates reflect the CO₂ costs that European manufacturers already have to bear as part of the EU Emissions Trading System(EU ETS).

The mechanism concentrates on emission-intensive industries such as steel, cement, fertilizers, aluminium and electricity. The focus is on industries that are particularly susceptible to carbon leakage.

Who developed the mechanism?

The CBAM (Regulation (EU) 2023/956) was introduced to prevent carbon leakage, i.e. the relocation of CO₂-intensive production to countries with less stringent climate protection requirements. The aim is to ensure that imported goods are subject to comparable CO₂ costs as products from the EU. At the same time, the mechanism sends a signal to trading partners to expand their own climate protection and CO₂ pricing systems.

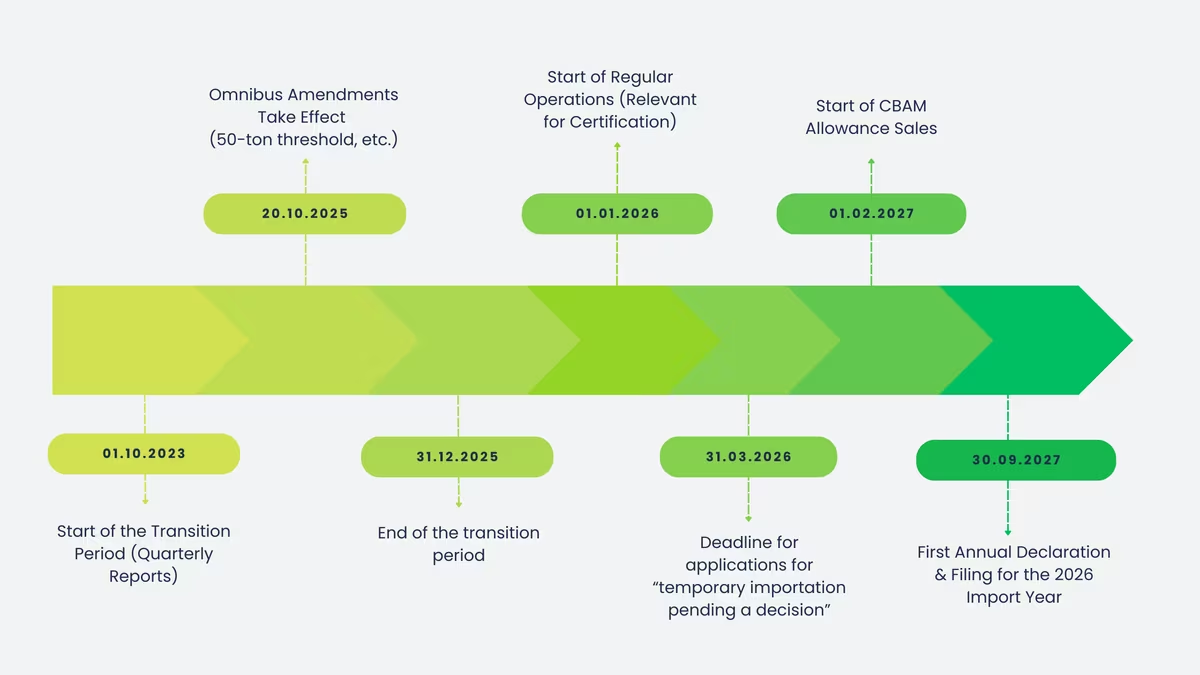

Since October 1, 2023, CBAM initially ran in a transitional phase with pure reporting obligations (without certificate purchase). This phase ended on 31 December 2025. The Carbon Border Adjustment Mechanism went into regular operation on 1 January 2026, albeit with simplifications from the amendment of October 2025: For many companies, a 50-tonne threshold now applies (cumulatively for aluminium, cement, fertilizers and iron & steel, among others). Only those above this threshold are subject to the full CBAM process and require the status of approved CBAM declarant.

The financial obligations will be implemented in stages: The sale of CBAM certificates will start on February 1, 2027 and the first annual declaration including submission for the import year 2026 is due by September 30, 2027.

The German Emissions Trading Authority (DEHSt) at the Federal Environment Agency is the authority responsible for implementing the CO₂ border adjustment system in Germany.

The main tasks of the DEHSt include

- Registration of importers: It manages the registration of companies that import goods subject to CBAM into the EU. This is done via the CBAM transitional register, which serves as an electronic portal for the submission of reports.

- Monitoring of reporting obligations: During the transition phase, importers were obliged to submit quarterly reports on goods imported into the EU and their embedded emissions. The DEHSt is responsible for receiving, reviewing and managing these reports.

- Communication with the European Commission: DEHSt acts as an interface between German importers and the European Commission to ensure that the regulations are applied uniformly.

- Implementation of correction and sanction procedures: In the event of irregularities or breaches of the regulations, DEHSt initiates procedures to ensure compliance with the regulations.

It is therefore essential for companies that import goods subject to CBAM to register with the DEHSt and submit the necessary reports on time in order to comply with the legal requirements.

Never miss an update on ESG & sustainability again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

How does the CBAM regulation differ from other climate protection instruments?

CBAM differs from many other climate protection instruments primarily in terms of where it starts: not in production within the EU, but at the border.

While CO₂ taxes, emissions trading or national climate laws are primarily aimed at pricing or limiting emissions domestically, the mechanism ensures that imported goods with a comparable CO₂ cost framework also enter the EU market. This is precisely how the mechanism addresses the central problem of carbon leakage, i.e. the relocation of emissions-intensive production to countries with less stringent climate protection rules, while at the same time stabilizing fair competitive conditions for companies that already bear CO₂ costs in the EU.

In contrast to the EU Emissions Trading Scheme (EU ETS), CBAM is not a separate system that caps the total amount of emissions. Instead, it works like a mirror mechanism: the CO₂ price is taken into account for selected, particularly emissions-intensive goods by basing the CO₂ costs for imports on the ETS price.

The difference is important: the ETS uses a market mechanism to control emissions within the EU, while CBAM primarily compensates for cost differences in imports and thus creates incentives to reduce emissions outside the EU or to set up CO₂ pricing systems.

Why was the CBAM introduced?

It was introduced because the EU can only credibly achieve its climate targets if CO₂ emissions are not simply relocated instead of reduced. Without a border adjustment, there is a risk that emissions-intensive production will migrate to countries with less stringent climate regulations and imports will then have a price advantage, even though they produce more CO₂.

This is precisely where the Carbon Border Adjustment Mechanism comes in: It ensures that CO₂ costs in the EU market are comparable, regardless of whether a product was manufactured in the EU or imported.

In short: the mechanism should...

→ Prevent carbon leakage: Emissions should fall, not migrate abroad.

→ Ensure fair competition: EU companies should not be structurally disadvantaged by CO₂ costs.

→ Initiate climate protection globally: Trading partners are given an incentive to expand their own CO₂ prices and climate standards.

→ Create transparency: The CO₂ footprint of imported goods becomes measurable and comparable, which strengthens controllability in supply chains.

When does the CBAM apply?

The border adjustment mechanism is not a one-off project, but a mechanism that was introduced gradually and remains a permanent part of EU climate policy. The crucial point in practice is the change in logic: from a pure reporting obligation to an annual compliance cycle with approval, declaration and certificate surrender.

Timetable for implementation (transition and full phase)

The introduction took place via a transition phase: since October 1, 2023, affected companies had to report quarterly, without financial obligation. This transition phase ended on December 31, 2025.

CBAM has been in regular operation since January 1, 2026. From this date, approval as an authorized CBAM declarant is central, as goods can only be imported via authorized declarants (or indirect customs representatives with corresponding approval). A CBAM declaration is required for this.

The staggered timing of the cash flow is important: the sale of certificates will not start until February 1, 2027, and the first annual declaration including submission for the import year 2026 is then due by September 30, 2027.

What will change during the transition phase?

During the transition phase, the main focus was on building up the data basis: Companies had to report on a quarterly basis which CBAM goods were imported and which embedded emissions were associated with them. There were explicitly no financial obligations in this phase; the focus was on learning, data quality and process development in the supply chain.

The effect: Those who have taken the transition phase seriously have a real advantage today (in regular operation) because CBAM will be less paperwork from 2026, but will have a direct impact on customs processes, purchasing, supplier management and ESG data flows in many companies.

What long-term effects are to be expected?

In the long term, the regulation will change three things:

- Supply chains are becoming more CO₂-sensitive. Emissions data is becoming a purchasing and competitive factor, not just a "nice to have", but increasingly a prerequisite for being able to deliver predictably in the EU.

- Decarbonization becomes more economical. The lower the carbon footprint, the lower the certificate burden, which creates incentives to invest in lower-emission production (including outside the EU).

- The scope can grow. In December 2025, the European Commission proposed extending CBAM to selected steel- and aluminum-intensive downstream products from 1 January 2028. This is still a proposal, but it clearly shows the direction: CBAM is intended to close along the value chain where carbon leakage risks can shift.

Aims of the CBAM

A key objective is to prevent carbon leakage, i.e. the relocation of CO₂-intensive production to countries outside the EU where CO₂ costs are lower or non-existent. Without such a mechanism, companies could relocate their production abroad in order to avoid the CO₂ price in the EU. This would undermine the EU's climate protection efforts and possibly even lead to an increase in global emissions. The CBAM ensures that climate protection measures within the EU are not undermined by loopholes on the global market.

The CO₂ compensation system should not only work within the EU, but also have a global impact on climate protection. By subjecting imports from countries with lower climate protection standards to CO₂ pricing, these countries are motivated to introduce their own CO₂ pricing systems and reduce their emissions. In this way, the Carbon Border Adjustment Mechanism supports the worldwide achievement of the climate targets of the Paris Agreement and contributes to limiting global warming.

Another aim is to ensure fair competition between European companies and their international competitors. As European producers already pay for their CO₂ emissions under the EU Emissions Trading System (EU ETS), the CBAM ensures that imports are not cheaper simply because of lower environmental standards. A level playing field strengthens domestic industry and ensures that companies are not disadvantaged by climate protection measures.

The revenue from the sale of CBAM certificates is to flow into sustainable projects that further promote climate protection within the EU. These funds could be used to finance innovations, accelerate the transition to a climate-neutral economy or support companies and households with decarbonization.

The customs duty aims to establish a globally harmonized pricing of CO₂ emissions in the long term. By implementing such a mechanism, global markets could be uniformly geared towards climate protection, which would make a decisive contribution to reducing global CO₂ emissions. This goal underlines the role of the European Union as a pioneering player in climate protection and points the way to an internationally coordinated and effective climate policy.

Which companies must comply with the CBAM?

CBAM is product-oriented. The decisive factor is therefore not the size of the company, but whether certain goods are released for free circulation from non-EU countries.

Since the amendment (in force since 20 October 2025), an important relief applies: a de minimis threshold of 50 tons net mass per calendar year (cumulative across these product groups) applies to aluminium, cement, fertilizers and iron & steel. Anyone who falls below this threshold is generally not subject to the obligations. This threshold expressly does not apply to electricity and hydrogen.

Since January 1, 2026, affected importers must also generally act as authorized CBAM declarants, otherwise the goods concerned cannot be imported regularly. This also applies if a company is not based in a member state: in this case, the import typically takes place via an indirect customs representative, who also requires the status of authorized declarant.

Significance for importers within the EU

For importers, CBAM will primarily be an operational compliance issue from 2026:

- Check affectedness

- Ensure approval

- Set up data streams for emission values

- Clarify internally who bears responsibility (purchasing, customs, sustainability, ESG, finance).

Important in the transition: Anyone who submitted the application for approval by March 31, 2026 was allowed to continue importing provisionally after the amendment until the authority had made a decision - this was the "safety anchor" to prevent supply chains from being interrupted by processing times.

Which countries and regions are indirectly affected?

Export countries and regions from which emissions-intensive goods are supplied to the EU are particularly affected indirectly, as CBAM changes pricing logic, verification requirements and therefore the competitive position of suppliers. This is particularly relevant for countries where carbon pricing is less pronounced: the pressure to provide reliable emissions data and to decarbonize their own production methods in order to remain competitive in the EU market is increasing.

At the same time, there are exceptions that are important for the classification: Imports from countries whose emissions trading is linked to the EU ETS or which participate in it (including Norway, Iceland, Liechtenstein and Switzerland) are generally excluded in this context. This shifts trade flows and benchmarks within individual sectors.

In practical terms, this means that CBAM not only affects importers in the EU, but also sends a signal along the supply chain, from producers in third countries to traders and processing industries in Europe that are heavily dependent on steel, aluminium, fertilizers or cement.

Which goods are affected?

The border adjustment mechanism deliberately starts where the climate levers are greatest: with particularly emission-intensive raw materials, which are at the beginning of many supply chains. The mechanism aims to reduce CO₂ emissions in these industries, not only through direct emissions from production, but also with regard to so-called gray emissions. In practice, this is often where the greatest need for data and evidence arises.

CBAM currently comprises six product groups or sectors. These include

- Iron and steel

- Cement

- Fertilizer

- Aluminum

- Hydrogen

- Electricity (power)

The specific goods covered are defined in detail in the regulation on CN codes (customs tariff numbers) (Annex I). In practice, this means that it is not the general description (steel, aluminum) that ultimately determines whether a product is CBAM-relevant, but the tariff classification.

They were specifically selected because they are emission-intensive and susceptible to carbon leakage.

Sectors of particular relevance

Steel production is one of the world's biggest CO₂ emitters, especially where blast furnaces are operated with coal. Accordingly, CBAM covers key products such as crude steel, rolled steel and steel pipes. The pressure for transformation is clear: lower-emission processes, such as hydrogen-based processes or electric arc furnaces, will become a decisive competitive factor in the future.

Cement is a key material in the construction industry and is also emission-intensive, not only because of the energy used, but also due to process-related emissions during clinker production. CBAM provides incentives to invest in lower-emission production methods and alternative binding agents in order to permanently reduce CO₂ intensity.

Aluminum is indispensable in many industries (automotive, packaging, mechanical engineering), but primary production is extremely energy-intensive. The mechanism includes primary aluminum and various semi-finished products (e.g. sheet metal, profiles). This makes the recycling lever particularly relevant: secondary aluminum generally has a significantly lower emissions footprint and is therefore strategically more important.

Fertilizers, especially ammonia-based products, produce high emissions (CO₂ and other climate-impacting gases). CBAM is intended to accelerate efficiency improvements and the switch to lower-emission production paths (e.g. green hydrogen/ammonia).

Electricity imports from fossil generation (coal/gas) may also be relevant. The aim is to reduce the distortion of competition compared to clean generation and to support the switch to renewable energies in the long term.

As an energy carrier and industrial input, hydrogen is central to decarbonization, but its emissions profile also depends heavily on the method of production. Inclusion in CBAM is intended to create transparency and provide incentives to strengthen low-carbon hydrogen along the supply chains.

Future extensions to the product lists: The scope is not static, and this is precisely what companies should keep in mind. In December 2025, the EU Commission proposed extending the scope to selected steel- and aluminum-intensive downstream products from 1 January 2028, i.e. goods that are further down the value chain (e.g. certain processed products). This is currently a proposal and therefore not yet finalized, but it clearly shows the direction: CBAM is intended to close the loop where carbon leakage risks can shift from raw materials to processed products.

How does the CBAM work?

CBAM essentially works like a CO₂ cost reconciliation for certain imported goods: Anyone importing goods into the EU must determine the embedded emissions of these goods and later, as part of the annual declaration, surrender the corresponding quantity of certificates.

The timing is important here: 2026 is the first import year in regular operation, but the purchase of certificates will not start until February 1, 2027.

CBAM certificates

Certificates are the central offsetting element in the system: they reflect the share of CO₂ costs that an EU manufacturer already bears via emissions trading and transfer this logic to imports. In practical terms, this means that the higher the emissions, the more certificates are required; the lower the footprint, the lower the burden. The quantity of certificates is based on the verified embedded emissions of the imported goods, minus eligible CO₂ costs in the country of origin (if verifiable and compliant).

How is the price of the certificates determined?

The price of the certificates is linked to the EU ETS price. Specifically, it is derived from the auction prices of EU ETS allowances. For imports in 2026 as a quarterly average, from 2027 generally as a weekly average. This is an important point of detail because, although 2026 already counts, the certificates cannot be purchased until 2027.

Acquisition of CBAM certificates

The purchase takes place via a central platform ("Common Central Platform"). Member states may only sell CBAM certificates from February 1, 2027. For companies, this means that they will prepare data, processes and quantity logic in 2026 and then procure the certificates from 2027 in order to meet the obligations for the import year 2026.

The system is supplemented by a hedging logic during the year: as a rule, importers must ensure that at least 50% of the required certificate volume is covered from regular operation onwards (reduced from 80% previously). This reduces the pre-financing pressure and makes the introduction much more manageable in practice.

In regular operation, the process can be described as an annual compliance cycle:

- Record imports (continuously throughout the year): Document quantities, goods classification (CN codes) and embedded emissions.

- Procure certificates (from February 1, 2027): Purchase via the central platform, i.e. downstream for the first import year 2026.

- Annual declaration & submission: The annual declaration must be submitted by September 30 of the following year; the required certificates must also be submitted by then (for the first time on September 30, 2027 for the import year 2026).

Differences between CBAM and ETS certificates

Even if the price logic is linked to the EU ETS, certificates are not the same as EU ETS certificates:

- EU ETS allowances are emission allowances for installations/companies that are regulated in the ETS; they can be traded and are part of a cap-and-trade system.

- CBAM certificates, on the other hand, are a specific instrument for imports: they are used for submission as part of the annual declaration and reflect the CO₂ costs for embedded emissions, linked to ETS prices, but functionally a separate compliance mechanism.

Registration and reporting obligations

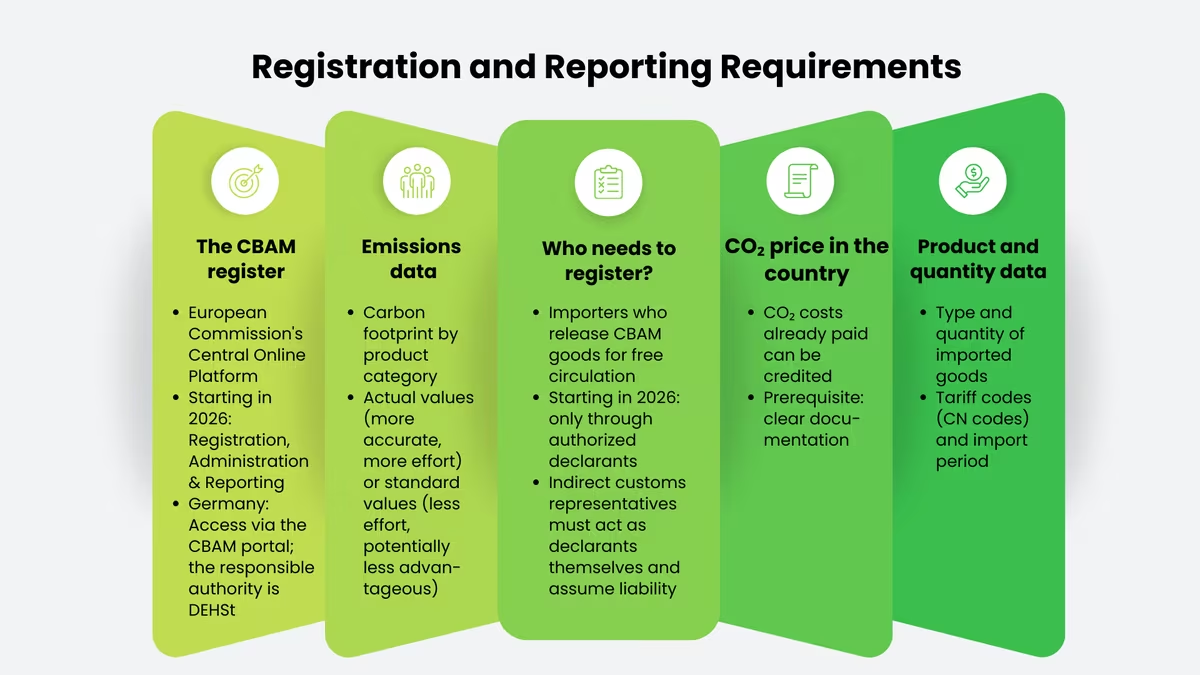

Anyone affected by CBAM will notice here at the latest: From 2026, the topic is no longer just reporting, but a clear compliance process: with approval, data requirements and fixed deadlines. The European Commission's CBAM register, which companies use to process their obligations and communicate with authorities, is the linchpin here.

What is the CBAM register?

The register is a standardized, secure online platform of the European Commission through which companies manage their obligations. During the transition phase (October 1, 2023 to December 31, 2025), it was primarily used to submit quarterly CBAM reports and enable communication between companies, national authorities and the Commission.

CBAM has been in regular operation since January 1, 2026, giving the register a much broader function: it is no longer just a reporting tool, but also the central system for authorization and administration. Importers and indirect customs representatives use the register to apply for authorized declarant status, which is crucial for imports from 2026.

For companies in Germany, access will continue to be via the customs portal or the CBAM portal for entrepreneurs, as was already the case during the transition phase. This is where access is technically managed and support is provided for entering the EU system. The responsible authority is the German Emissions Trading Authority at the Federal Environment Agency. It monitors the process, checks information, coordinates with the Commission and can initiate corrections or procedures in the event of discrepancies.

Who needs to register?

Importers who release goods from non-EU countries for free circulation must register. From 2026, the following applies: affected imports may only be made via authorized declarants. Anyone who falls above the relevant threshold will need a valid authorization.

Particularly important: Indirect customs representatives are not only technical processors, they must themselves act as authorized declarants and therefore assume full responsibility in the process. It is therefore worth clarifying at an early stage who will take on which tasks: Purchasing, Customs, ESG, Finance and external partners.

What data must be reported?

The border adjustment mechanism is essentially a data and verification process. It is not only the quantities and types of goods that are decisive, but above all the embedded emissions (i.e. the carbon footprint of the imported goods). To achieve this, companies must set up their supply chain in such a way that the relevant information is reliably available, ideally directly from the manufacturer.

Typically, companies need three data blocks for this:

- Goods and quantity data

What goods were imported, in what quantity, under what customs tariff numbers (CN codes) and in what period? - Embedded emissions data

The embedded emissions per product group, either on the basis of actual emission values or, where permissible or sensible, on the basis of default values. In practice, it is precisely here that the level of effort required is decided: Real values are more precise, but require more supplier involvement and possibly verification processes; default values reduce effort, but can be less advantageous in terms of crediting and control. - CO₂ price in the country of origin

If a CO₂ price has already been paid in the country of origin, this may be relevant for subsequent invoicing, but only if it can be properly verified or can be offset within the scope of the intended logic.

Deadlines and consequences of non-compliance

The deadlines differ depending on whether you are still talking about the transitional logic or are already in regular operation. Although the transition phase expires at the end of 2025, it is important in practice that the last quarterly report (Q4/2025) must still be submitted on time. From regular operation onwards, the focus shifts to the annual declaration and the later submission of certificates.

As a rule, companies must submit the annual declaration on time and organize the necessary processes so that emissions data is complete, plausible and verifiable. Anyone who is late or provides incorrect information risks correction procedures and, depending on the violation, sanctions. Indirect customs representatives can also be affected if they take on duties and do not fulfill them properly. The bottom line is that CBAM is not an issue that runs alongside the customs process, but requires clear responsibilities and clean data chains.

Opportunities and challenges

Carbon offsetting offers companies a wide range of opportunities, especially for those who adopt sustainable strategies early on. The focus on climate protection and fair competition creates new opportunities for innovation, market positioning and long-term planning. Despite its benefits, the mechanism also poses risks and challenges for companies, international trade relations and developing countries. In order to deal successfully with the mechanism, companies must adapt to the changes at an early stage. We summarize the key risks and examples below:

Opportunities

Incentive for sustainability: The mechanism encourages European companies to make their production processes more sustainable. This concerns both the introduction of energy-efficient technologies and the use of low-emission raw materials. An example of this is the development of green steel through the use of hydrogen instead of coal in steel production. The aim of this is to reduce costs for CO₂ certificates and at the same time secure market share through innovative products.

Promotion of key technologies: Companies that develop and use technologies with low CO₂ emissions can gain a competitive edge. These technologies not only make companies more competitive, but also help to set new standards for the entire industry. Examples include low-emission cement production using alternative binding agents and recycling processes in the aluminum industry.

Sustainability sells itself: CBAM strengthens the demand for sustainably produced goods. Companies that can demonstrate environmentally friendly production processes have a competitive advantage - both within the EU and on international markets. Sustainability is increasingly becoming a key factor for consumers and business partners, and companies are now benefiting from this.

Pioneering role in climate-friendly production: Companies that switch to climate-friendly production at an early stage can position themselves as pioneers of sustainability. This not only strengthens their image, but also their negotiating position in international markets.

Clarity on CO₂ costs: The carbon border adjustment establishes a standardized system that supports companies in more accurately estimating the expenses for CO₂ emissions in global trade. This clarity promotes long-term planning and enables companies to make targeted strategic investments.

Investing in climate-friendly technologies: A clearly defined framework for carbon pricing allows companies to invest more confidently in innovative solutions and technologies, which will both reduce costs and give them a competitive advantage in the long term. Examples of this include switching to renewable energy sources or updating production facilities.

Fair competition: The border adjustment system ensures that European production sites are protected against unfair competition from imports from countries with lower environmental standards. This is intended to strengthen the domestic economy and create incentives to expand production capacities within the EU.

Promoting regional supply chains: In view of rising import costs, local and regional supply chains are becoming increasingly important. This could contribute to increased value creation within Europe and reduce dependence on external countries.

Challenges

Complexity of data collection: Companies must prepare and submit detailed reports on the CO₂ emissions of their imported products. An example of this is a company that imports steel from a non-EU country. It must analyze the entire production process in order to calculate the exact emission values. The challenge here is that if suppliers provide incomplete or incorrect data, there is a risk of additional costs due to the use of default values.

New reporting obligations: The introduction of CBAM requires additional resources for compliance with reporting obligations and the establishment of corresponding systems. One example of this is small and medium-sized companies, which may have difficulties bearing the costs of additional compliance departments.

Financial burden for importers: The purchase of certificates increases the import costs for products that originate from countries with lower climate protection requirements. An example of this is a construction company that purchases cement from a third country. It has to factor in the additional CO₂ costs, which has an impact on the overall costs of construction projects. The challenge here is that these costs could be passed on to end customers, reducing demand for such products.

Investment required for conversions: Companies may need to invest in new technologies in order to remain competitive. One example here is an aluminum manufacturer that could dispense with energy-intensive recycling processes and introduce lower-emission processes instead, but this would require high levels of investment.

Resistance from trading partners: Countries without comparable CO₂ pricing systems could view border adjustment as a protectionist measure and initiate countermeasures. For example, the USA and China have already expressed concerns and could impose tariffs on European exports. This could exacerbate trade conflicts and strain relations with important trading partners.

Regulatory uncertainties: International organizations such as the WTO examine whether the CBAM is compatible with the rules of free world trade. For example, a WTO dispute could delay implementation and create uncertainty for companies.

Disadvantage for exporting countries: Developing countries whose industries rely heavily on exports to the EU could be significantly burdened by the additional costs. For example, a country that exports aluminium or fertilizers could lose market share to lower-emission competitors. These countries often do not have the financial resources or technology to convert their production quickly.

Risk of economic disparities: The additional expenditure could restrict exchange between the EU and developing countries, which would hinder their economic progress.

Unclear effects: During the test phase from 2023 to 2026, it remains unclear to what extent the CBAM will actually have an impact on companies and trade players. For example, companies may find it difficult to factor long-term costs into their strategic planning. The uncertainty could delay investments and make strategic decisions more difficult.

Expansion to other sectors: The prospect of extending carbon offsetting to other sectors in the future could pose a potential challenge. For example, the chemical industry or the food sector could be affected by future regulations without clear guidelines.

Influence on the supply chain

The Carbon Border Regulation will fundamentally change the structure of global supply chains. Companies will have to reanalyze their sources of supply and give preference to partners from countries with comparable climate protection standards. At the same time, diversification is becoming increasingly important in order to mitigate risks such as trade disputes or unexpected costs.

Regional value chains and European suppliers are coming more into focus. Suppliers who invest in low-emission technologies are preferred in the long term - sustainability is thus becoming a decisive competitive criterion. Companies are increasingly demanding precise carbon footprints and evidence along the entire supply chain.

Logistics is also affected: Lower-emission means of transportation and shorter transport routes are becoming more relevant, while rising costs can have an impact on end prices.

Companies that focus on sustainable supply chains at an early stage can strengthen their market position and be perceived as pioneers.

Effects on various sectors

CBAM primarily affects emissions-intensive industries - both through certificate costs and through new requirements for verification and reporting. At the same time, it creates incentives for innovation and more sustainable production.

Steel: The steel industry is one of the largest CO₂ emitters, primarily due to the use of coal in blast furnaces. Imported steel from countries such as China, India or Turkey is becoming significantly more expensive due to certificate costs. At the same time, there are incentives for low-emission technologies such as electric arc furnaces or green hydrogen.

Cement: Cement production causes high emissions - both through energy consumption and chemical processes. Cost increases for imports from third countries are affecting an industry that is already difficult to decarbonize. Carbon capture technologies and alternative binders offer long-term potential.

Aluminum: Aluminum production is particularly emission-intensive due to its high energy consumption. The dependence on imports of primary aluminum - from Russia or Canada, for example - makes supply chains considerably more expensive. Aluminum recycling within the EU is therefore gaining in importance as a significantly lower-emission alternative.

Fertilizers: The use of fossil fuels makes fertilizer production a significant CO₂ emitter. Rising import costs are an additional burden for European farmers. Switching to green ammonia offers a promising, but currently still costly alternative.

Electricity: Electricity imports from coal or gas-fired power plants fall directly under CBAM and will become significantly more expensive. This increases the pressure on energy companies to adapt their supply chains and at the same time promotes investment in renewable energies and cross-border cooperation in the field of clean energy.

Future developments

With the potential expansion of the carbon tariff to additional sectors such as the chemical industry, paper production or the food sector, the influence of this mechanism will continue to grow in the coming years. Companies that invest early in sustainable practices and low-emission technologies can see this challenge as an opportunity to establish themselves as pioneers in climate protection in the long term. The CBAM is forcing different industries to adapt their business models to the requirements of a climate-neutral economy while maintaining their global competitiveness.

CBAM and international competitiveness

CBAM influences the international competitiveness of European companies on several levels, both positively and negatively. A strategic examination of the mechanism is therefore essential.

Opportunities

Fair competitive conditions: The mechanism ensures that imported goods are subject to the same CO₂ costs as goods produced in the EU. This prevents emissions-intensive imports from unfairly displacing European products:

- Products from countries with lower environmental standards can no longer be offered at artificially low prices

- European companies that are already investing in sustainable technologies are specifically protected from unfair competition

CBAM does not create a barrier to trade - it creates fairness.

Innovation incentives: The mechanism rewards companies that adopt low-emission production methods at an early stage:

- Climate-friendly production avoids certificate costs and achieves long-term efficiency benefits

- Examples such as green hydrogen in the steel industry or alternative binders in cement production show where the journey is heading

- Sustainability is increasingly becoming a decisive competitive advantage on global markets - for consumers and business customers alike

Investing in climate-friendly technologies now will save certificate costs tomorrow.

Global signal effect: CBAM has an impact beyond the EU:

- Trading partners are motivated to introduce their own CO₂ pricing systems to avoid additional costs for EU exports

- The mechanism can serve as a model for other regions and initiate international harmonization of climate protection standards

Challenges

Higher production costs: Strict EU climate regulations mean higher costs - and this is not without consequences:

- This can weaken export capabilities, particularly in price-sensitive sectors such as steel, cement and aluminum

- Companies in third countries without comparable climate regulations often produce more cheaply and therefore remain more attractive on global markets

Climate protection has its price - CBAM should ensure that not only Europe pays it.

Trade conflicts: CBAM is perceived by some countries as a protectionist measure:

- The USA, China and India have already commented critically on the mechanism

- There is a risk of retaliatory measures such as punitive tariffs, which could hit European exporters hard

- Existing trade relations could come under pressure as a result

Export markets under pressure: Rising production costs can weaken the competitive position on international markets:

- In price-sensitive markets, customers could switch to cheaper alternatives outside the EU

- Trading partners who feel disadvantaged could diversify their supply relationships at the expense of European export volumes

Strategies for companies

In order to adapt effectively to the CO₂ border tax, companies should carry out a comprehensive analysis of their supply chain. This should include determining the carbon footprint of manufactured products at every stage of production and transportation. The aim is to identify emission-intensive processes and optimize or replace them if necessary. Such an analysis makes it possible to replace emitting materials and integrate alternative, more sustainable raw materials into the production process.

Companies should actively invest in sustainable technologies. These include energy-efficient devices and systems that both minimize resource consumption and reduce emissions. The use of renewable energies, such as solar panels or wind power, can also make a significant contribution to reducing CO₂ emissions. In the long term, such investments not only lead to a reduction in emissions, but also to cost savings through lower energy costs.

Employee training and awareness-raising on sustainability and adaptation to CBAM should not be ignored. Training can help raise awareness of environmentally friendly practices and empower employees to actively contribute to reducing the company's carbon footprint.

The introduction of a transparent system for sustainability reporting is also important. Companies are required to provide regular information on their progress in reducing CO₂ emissions and the associated measures. This also includes reporting on measures to comply with carbon offsetting. Companies that report on CBAM not only promote credibility, but also gain a competitive advantage to attract stakeholders willing to invest.

Another strategy is to collaborate with other companies and stakeholders within the industry. By sharing best practices, experiences and resources, companies can learn from each other and develop joint solutions that further minimize CO₂ emissions. Networks to promote sustainability can play a supporting role here.

The role of technology in the implementation of CBAM

Data analysis and management

Technological solutions for data collection and analysis are necessary to effectively measure and manage the environmental footprint. With the help of software tools, companies can collect and analyze accurate data on their energy consumption, emissions and material flows. This information is essential to make informed decisions to reduce direct and indirect emissions and ensure compliance.

Automation of processes

Production and logistics processes can be made more efficient through the use of modern automation technologies. Automation can not only stop material waste, but also reduce energy consumption in production. For example, the intelligent control of machines and systems can optimize operations and minimize energy consumption at the same time.

Integration of artificial intelligence (AI)

The use of AI technology can help companies make predictive decisions to minimize CO₂ emissions. AI can be used to develop knowledge databases to optimize material selection and production processes. Machine learning can be used to identify patterns that indicate optimization potential in the supply chain.

Support with compliance requirements

Technological solutions can also help companies to comply with the regulations. Special software solutions help to collect and process all the data required to comply with CO₂ limits. Companies are thus able to continuously monitor and adapt current information on emissions-related regulations and requirements.

Platforms for the exchange of best practices

Technologies can also promote the exchange of best practices and experiences between companies. Through online platforms and networks, companies can share knowledge about emission-reducing practices, offer training or initiate innovation projects that contribute to CBAM compliance.

Adapting to the Carbon Border Adjustment Mechanism requires a strategic approach and the use of modern technologies. Companies that proactively invest in evaluating their supply chains, adopt sustainable technologies and train their employees can not only reduce their environmental footprint, but also strengthen their competitiveness in the market.

The use of technological solutions for data collection, process automation, AI and compliance management plays a crucial role in the implementation of these strategies. The combination of innovative approaches and a clear objective will enable companies to successfully master the challenges and make a positive contribution to sustainability at the same time.

Conclusion

CBAM is an important step in climate policy: it creates fair competitive conditions, promotes low-emission technologies and provides incentives far beyond the EU. Exporting companies worldwide must adapt their standards. At the same time, the mechanism opens up opportunities for international cooperation and global harmonization of CO₂ prices.

Companies that act proactively not only fulfill regulatory requirements, but also position themselves as pioneers of a more sustainable economy. CBAM could thus initiate a fundamental change, characterized by innovation, collaboration and a clear focus on sustainability.

Frequently asked questions

The Carbon Border Adjustment Mechanism is an instrument of the European Union that was developed to address one of the most pressing challenges in the field of climate protection: the risk of carbon leakage. This risk occurs when companies are tempted to relocate their production to countries with lower environmental standards and lower or no CO2 prices in order to reduce their costs. As a result, not only would environmental protection targets in the EU be undermined, but the competitive conditions for European companies that adhere to strict climate regulations would also be reduced.

The mechanism was introduced to support EU climate targets by ensuring that European manufacturers subject to strict environmental regulations are not disadvantaged compared to imported goods from regions with less stringent CO2 requirements.

Sectors with high CO2 emissions are affected first. This includes the following products and sectors:

- Steel and iron: These materials are basic materials for numerous industries and have high CO2 emissions during production.

- Aluminum: Aluminum production is energy-intensive and contributes significantly to greenhouse gas emissions.

- Cement: Cement is a key building material whose production is associated with high CO2 emissions.

- Fertilizers: The production of nitrogen fertilizers leads to considerable emissions, especially when fossil fuels are used.

- Electricity: Imported electricity generated from fossil fuels is also included under CBAM to ensure that energy imports are subject to the same CO2 prices as electricity generated in the EU.

- Hydrogen: Hydrogen produced from fossil fuels with high CO2 emissions also falls under CBAM, especially if it is to be imported on a large scale.

- Industrial chemical products: Other chemical products that are considered energy-intensive or cause high CO2 emissions during their production.

It is expected that the list of products covered by CBAM will be expanded over time, especially as more sectors are identified that also cause significant CO2 emissions. The regulations may also adapt to advances in climate policy and technological development.

Importers must make a payment that corresponds to the CO2 price paid by European companies. The aim is to ensure fair competition for European producers.

The obligation to purchase certificates is primarily aimed at importers of goods that enter the EU and fall under the applicable regulations.

- Importers: Companies or individuals who import goods from third countries into the EU. This applies to all affected products imported into the EU, especially those from sectors that cause high CO2 emissions, such as steel, aluminium, cement, fertilizers, electricity and hydrogen.

- Dealers and distributors: Retailers who import these products as part of their business activities must also purchase the relevant certificates and report the associated CO2 emissions.

Importers must buy certificates that correspond to the CO2 emissions generated in the production of the imported goods. The price of these certificates is linked to the CO2 price in the EU. They are also obliged to submit regular reports on the quantity of imported goods and the associated CO2 emissions. This reporting serves to ensure transparency and to monitor compliance with the requirements by the EU authorities. Companies must keep records and documentation to prove the origins of the imported goods and their production methods. This is crucial in order to prove how high the CO2 emissions were during production.

CBAM can help companies to develop more sustainable production methods in order to avoid competitive disadvantages. It can also increase the demand for environmentally friendly products.

Life cycle analysis (LCA) is a comprehensive method for calculating CO₂ emissions that takes into account all phases of the product life cycle. This includes the procurement of raw materials, where emissions from the extraction of materials are recorded, the production phase with emission-specific data from the production sites and the transportation of the product. This holistic approach enables companies to precisely quantify their environmental impact and take targeted measures to reduce it.

Another method of calculating emissions is via emission factors. These are specified values that describe the amount of CO₂ per production unit or product. These factors vary depending on the production technologies used and the energy sources used, such as gas, coal, oil or renewable energies. The EU provides standardized emission factors, while importers can also provide their own detailed evidence.

In order to calculate CO₂ emissions accurately, importers are obliged to provide comprehensive documentation and evidence. This includes certificates that prove the origin of raw materials and their environmental certifications. In addition, the manufacturer must provide production data that indicates the CO₂ emissions generated during production. Proof of transportation is also required, which provides information on the means and routes used to transport the goods to the EU.

The mechanism primarily affects countries and regions that could export, particularly in sectors that generate high CO₂ emissions. The introduction of this mechanism has a particular impact on countries whose environmental standards and CO₂ prices lag behind those of the EU.

Many emerging and developing countries, such as China and India, face challenges from the Carbon Border Adjustment Mechanism. These countries often have less stringent environmental regulations and use less expensive production methods, which could make it more difficult for them to export products to the EU, particularly goods such as steel, cement or fertilizers.

Some industrialized nations that have lower CO₂ prices or less stringent environmental regulations in certain areas could also be affected. These include Russia and the United States.

Some regions that are heavily dependent on fossil fuels or whose industrial activities cause high emissions will also be affected, such as Central and Eastern Europe and South East Asia.

Yes, companies importing affected goods will need to adapt to CBAM and may need to adjust their supply chains and production methods to meet the new requirements.

Monitoring is carried out by the EU authorities, who ensure that the imported goods comply with the requirements. Specific implementation is supported by reporting obligations and transparency mechanisms.

If companies do not comply with the requirements, they can expect various legal and financial consequences. The exact sanctions and measures depend on the severity of the violations and the specific rules and regulations laid down by the EU and the competent national authorities. This can result in financial penalties such as fines, administrative penalties such as extended penalties or loss of registration, as well as reputational damage.

CBAM could lead to an intensified global discussion about CO2 prices and environmental standards. Countries could be forced to rethink their own climate protection measures in order to remain competitive in international trade.

Companies should conduct a comprehensive analysis of their supply chains to identify potential risks and opportunities associated with CBAM and adapt their strategies accordingly.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.