Important facts

- What is double materiality?

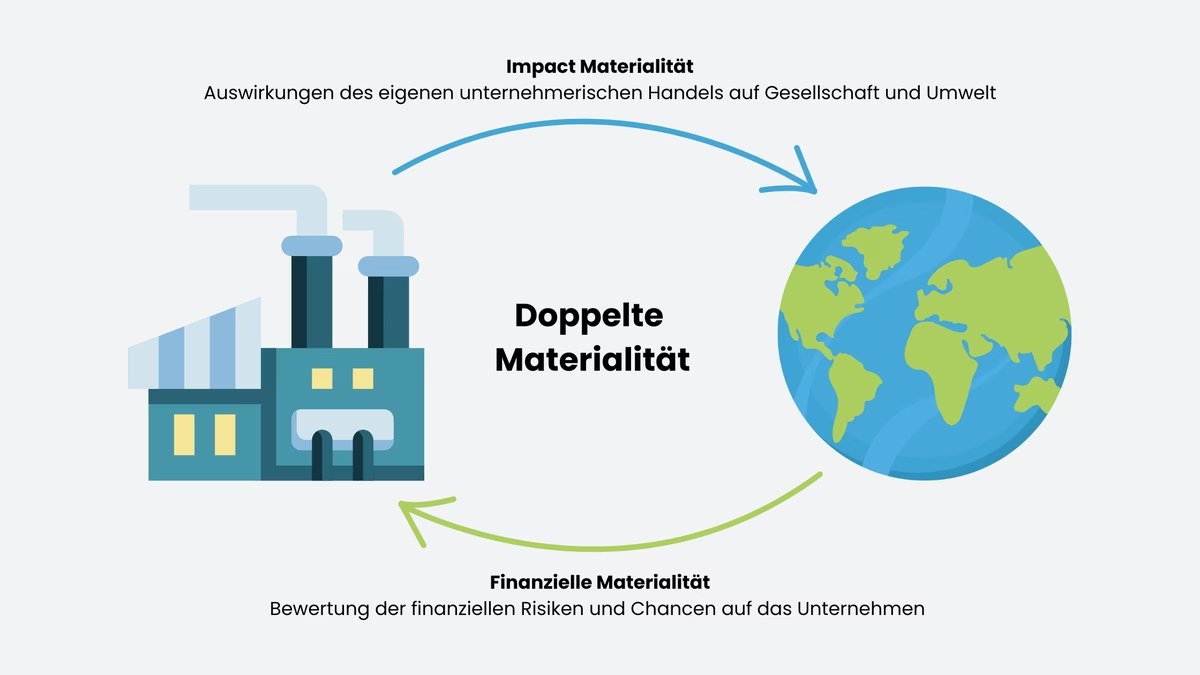

- Dual materiality is a central principle of ESG reporting, which takes into account both the company's impact on the environment and society and the risks to the company.

- What is impact materiality?

- The focus here is on the company's impact on the environment, society and human rights.

- What is financial materiality?

- Assesses how ESG factors can influence the company's financial position and performance.

- Where is it prescribed?

- It is anchored in the CSRD and is a mandatory component of the ESRS reporting obligations.

- Why is it important?

- It provides a holistic view of sustainability, combines corporate responsibility and risk management and serves as the basis for transparent ESG reports.

- What do companies need to do?

- You must carry out a materiality analysis of both perspectives, identify and document relevant topics and integrate the results into the sustainability report.

Abstract

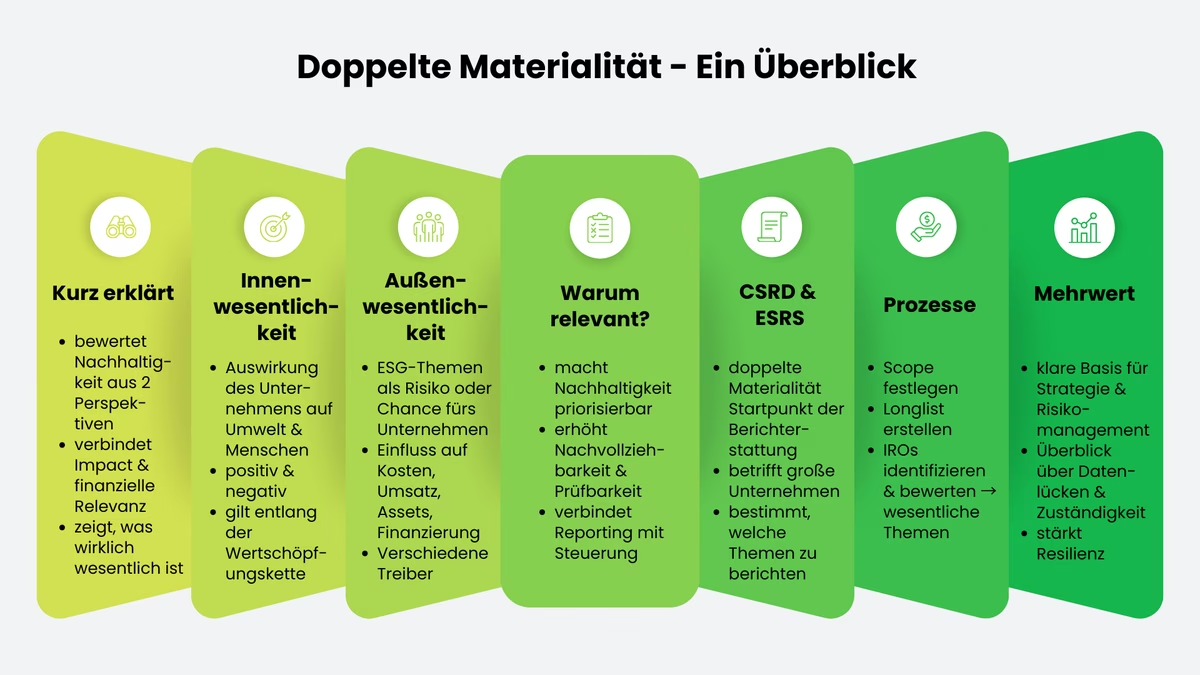

Double materiality looks at sustainability from two perspectives: What impact a company has on the environment and society (impact materiality) and which ESG issues have a financial impact on the company as risks or opportunities (financial materiality). With CSRD and ESRS, the dual materiality analysis becomes mandatory for many companies, especially for large companies and later partly also for capital market-oriented SMEs.

The process is clearly structured: define the scope, collect topics, assess impacts, risks and opportunities and derive the material topics, ideally with the involvement of relevant stakeholders. Even if this is time-consuming, it helps companies to sharpen their reporting and strengthen their sustainability strategy in the long term.

Double materiality: definition and background

What is double materiality?

Double materiality means that sustainability issues are assessed from two perspectives. It is therefore not only about what is financially relevant, but also about what impact the business activity has on the environment and society. This is exactly what the two terms " internal materiality " and " external materiality" stand for:

Inside materiality (also: impact materiality or inside-out perspective) refers to the consideration of the actual and potential impacts that a company has on people and the environment through its activities, products and services and along the entire value chain. This includes both negative and positive effects, for example on climate change, biodiversity, working conditions or consumer concerns.

Financial materiality (also known as the outside-in perspective) looks in the other direction: which sustainability issues have an impact on the company? The question here is whether environmental or social developments, new regulations or changing market requirements become risks or opportunities and thus influence the business model, financial situation or future earnings.

The decisive factor here is that an issue can be material from only one of the two perspectives or from both at the same time. It is precisely this dual approach that enables a more comprehensive prioritization and prevents companies from treating sustainability either only as an "impact issue" or only as a "financial issue".

Background: how did the concept come about?

The dual materiality has become so important in recent years because it better reflects how companies are managed today. In the past, sustainability reporting was often strongly characterized by voluntary CSR approaches and was therefore primarily a question of responsibility towards the environment and society. Nowadays, however, what counts most are reliable, comparable and verifiable statements. Stakeholders, from investors and customers to employees and authorities, want to know which topics are really relevant, how companies have assessed them and what they have derived from them in concrete terms.

With the CSRD and the ESRS, this development is picking up speed once again. Dual materiality is becoming the starting point for reporting because it acts as a filter to determine which topics a company really needs to present in depth and include in its management. Internal and external materiality are not two separate areas: What a company triggers in the environment and society can translate into risks or opportunities over time, for example through stricter regulations, reputational pressure, changes in demand or higher costs in the supply chain. Conversely, climate risks or scarce resources show how strongly external sustainability factors now influence very specific economic decisions.

The dual materiality helps companies to maintain an overview: It shows which sustainability topics are really important and how to sensibly link reporting obligations with strategy, risks and responsibilities within the company.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Timetable for first-time application (as at February 2026)

As part of the "stop-the-clock" regulation, the application of the CSRD was postponed by two years for companies in later waves. This means that the following applies to first-time sustainability reporting:

- Wave 1 (already subject to NFRD/CSR-RUG): Financial years from January 1, 2024 → report on 2024, publication typically 2025.

- Wave 2 (other large companies): Financial years from January 1, 2027 → report on 2027, publication typically in 2028.

- Wave 3 (listed SMEs): Financial years from January 1, 2028 → Report on 2028, publication typically in 2029.

Impact materiality and financial materiality

With CSRD and ESRS, two perspectives are particularly in focus with regard to dual materiality: outside-in/financial materiality and inside-out/impact materiality. Both pose different questions, but in practice they belong together. This is because sustainability works in both directions: Companies influence the environment and society - and conversely, ecological and social developments are increasingly influencing the business model, risks and economic decisions.

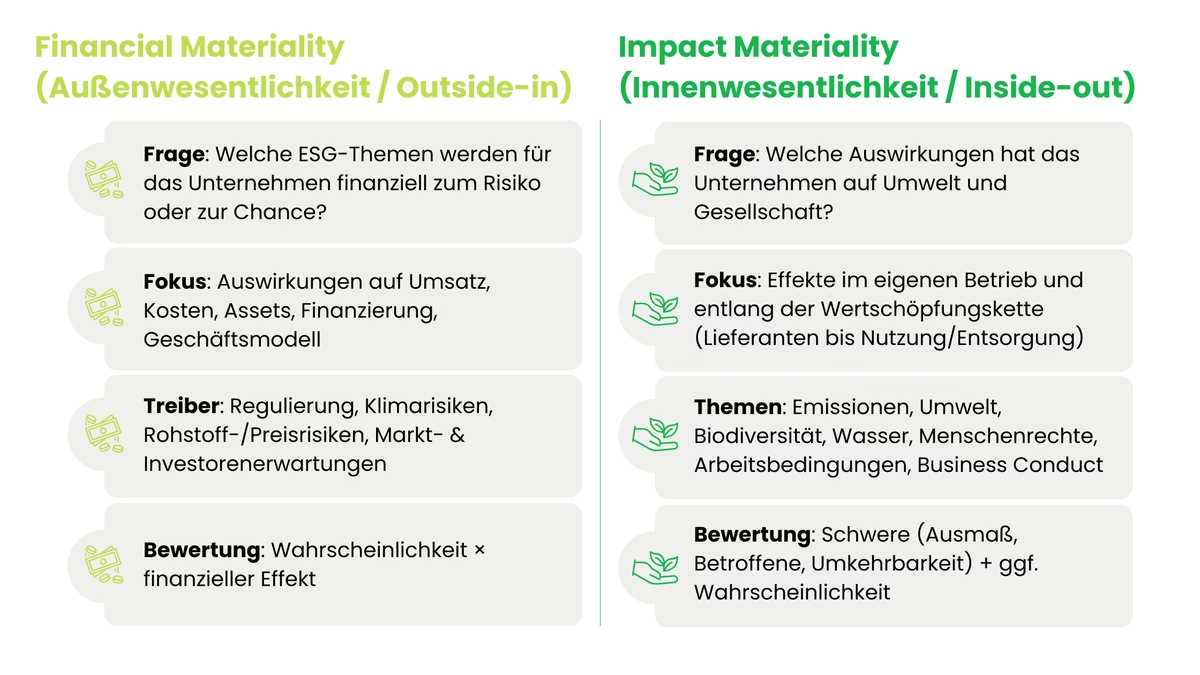

Outside-in approach: external materiality

External materiality means: Which sustainability issues can harm or benefit the company financially? It is therefore about which external developments become risks or opportunities, for example for sales, costs, assets, financing or long-term competitiveness. Triggers can include new laws and political requirements, physical climate risks such as extreme weather or water scarcity, but also the availability of raw materials, price trends and rising expectations from customers, investors or banks.

The decisive factor here is not just whether an issue is "somehow relevant", but how realistic it is that it will occur and how great the financial effect would be. External materiality is therefore closely linked to the classic risk and management system in the company, but expands it to include sustainability issues that have often not been properly recorded to date.

Inside-out approach: internal essentiality

Internal materiality looks in the other direction: what impact does the company have on the environment and society? This involves positive and negative effects in the company's own operations, but also along the entire value chain: i.e. with suppliers (upstream) as well as with the use and disposal of products (downstream). Topics can include emissions and environmental pollution, biodiversity and water, working conditions and human rights, as well as corruption prevention and responsible corporate governance.

What is important is that it is not only what is already visible today that counts, but also what impacts could plausibly arise in the future. The main factors assessed are the severity of an impact, i.e. how big it is, how many people are affected and whether it can be reversed. In the case of possible impacts (that have not yet occurred), the question of how likely they are is also added. This makes it clear where a company really bears responsibility - even if this is not immediately expressed in euros and cents.

Practical implementation: double materiality

In practice, internal and external materiality are often closely related, but they are not the same thing. The negative effects caused by a company can also have a financial impact later on, for example through stricter regulations, lawsuits and legal costs, reputational damage, delivery failures or because customers and banks drop out. Conversely, external developments such as new laws, changing markets or increasing climate risks can lead to companies having to adapt their strategy, for example by replacing materials, changing processes or imposing stricter requirements on suppliers. This is precisely why CSRD requires a dual perspective: it brings both together - what the company does externally and what has an impact on the company from the outside.

When companies consider financial and impact materiality together, a solid basis is created for the materiality assessment according to ESRS. They can clearly prioritize why certain topics are material and derive which standards and disclosures in the sustainability report are really relevant. At the same time, the process also brings internal benefits: It makes risks, opportunities and impacts more transparent, clarifies responsibilities and helps to link sustainability issues neatly with strategy, governance and risk management.

Create CSRD report

Our guide will show you how to create a sustainability report step by step.

Performance of the materiality analysis

With CSRD and ESRS, the dual materiality analysis becomes the starting point for sustainability reporting. It determines which topics a company really needs to report on in depth in accordance with ESRS - and at the same time helps to integrate these topics into strategy, risk management, processes and data management. The aim is to systematically record and comprehensibly evaluate material impacts as well as risks and opportunities (IROs) and to derive from this which ESRS disclosures are relevant.

Why the materiality analysis is so important

The materiality analysis is more than just a formal starting point. It is the filter logic that prevents companies from reporting "into the blue". Instead, it makes it possible to justify why certain topics are prioritized and what consequences follow from this, for example for data points, responsibilities or measures.

In practical terms, this means that a reliable analysis helps,

→ prioritize relevant topics (instead of treating all topics equally),

→ identify gaps in data and processes at an early stage,

→ set up roles and responsibilities consistently,

→ plan IT and reporting structures in a targeted manner,

→ and link the results to strategy and risk management.

What is specifically evaluated in the analysis

Two perspectives are considered in parallel in the dual materiality:

Inside materiality (impact / inside-out):

- What actual or potential impact does the company have on the environment and people, in its own operations and along the value chain?

External materiality (financial / outside-in):

- Which sustainability issues create risks or opportunities for the company, for example for the business model, costs, sales, assets, financing or reputation?

Important: A topic can only be material from one perspective or from both. This is precisely what makes the logic connectable for reporting and management.

A well-designed materiality analysis typically results in:

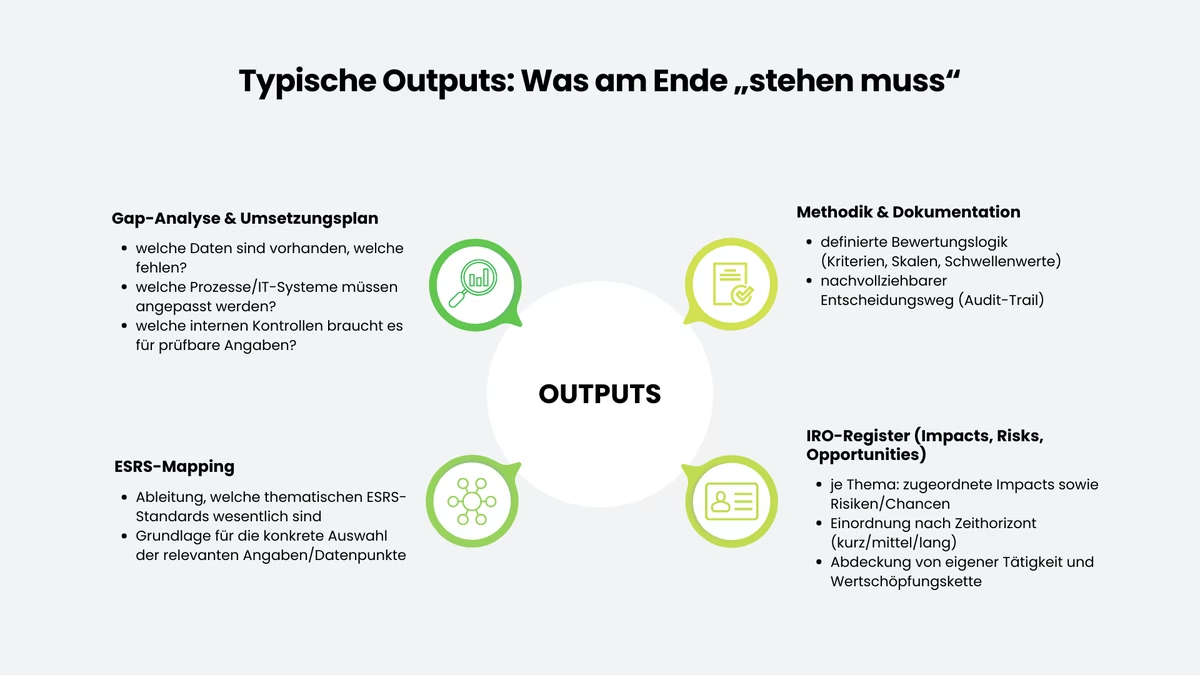

Typical outputs: What "must" be at the end

- Defined evaluation logic (criteria, scales, threshold values)

- Comprehensible decision-making process (audit trail)

- per topic: assigned impacts and risks/opportunities

- Classification by time horizon (short/medium/long)

- Coverage of own activities and value chain

- Derivation of which thematic ESRS standards are essential

- Basis for the specific selection of relevant information/data points

- Which data is available, which is missing?

- Which processes/IT systems need to be adapted?

- What internal controls are needed for verifiable information?

This makes it clear that the materiality analysis is not just an "analysis", but also provides the blueprint for the entire reporting setup.

Important note: At the same time, the CSRD is being revised in terms of content and scope as part of the omnibus/simplification package (including significantly higher thresholds). As a result, reporting obligations for individual companies may shift or cease to apply, depending on whether they still fall within the scope in future.

ESRS and the double materiality

The ESRS make dual materiality the basis for sustainability reporting. ESRS 1 stipulates that companies must base their disclosures on a comprehensible materiality assessment. It therefore serves as a "filter" to determine which topics are really dealt with in depth in the report. EFRAG's Implementation Guidance IG 1 provides helpful, albeit non-binding, guidance for practical implementation.

How this filter logic affects the standards is particularly important for reporting: Disclosures in accordance with ESRS 2 (General Disclosures) generally apply to all reporting companies. The thematic standards are generally only reported if the respective topic has been identified as material. A special justification logic applies to the topic of climate change (ESRS E1): if E1 is classified as not material in its entirety, this decision must be explained in a particularly plausible manner.

Implementation of dual materiality

For dual materiality to work in practice, a clear process is needed that looks at both sides: What impact does the company have on the environment and people and which ESG issues become a risk or an opportunity for the company. The end result should not just be a list of "material topics", but results that can be used directly for further work: a simple description of the approach, an overview of impacts, risks and opportunities (IROs), a decision on which ESRS topics need to be reported and a plan of which data, processes and responsibilities are still missing.

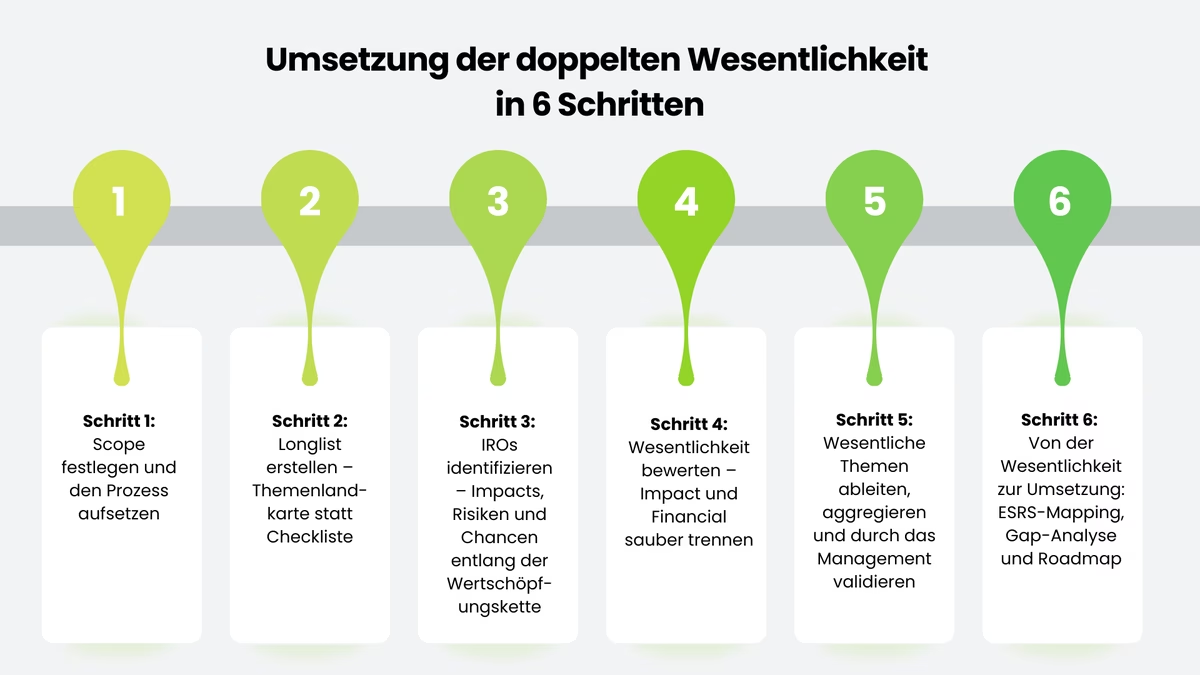

How to implement dual materiality

Before starting the materiality analysis, the company should first define the framework. This includes an overview of the most important activities, products and locations and also what the value chain looks like, i.e. from the suppliers to the use and disposal of the products. It is also worth considering external factors, such as new regulations, market requirements, industry-specific risks or information from the media, NGOs and benchmarks.

It is at least as important to define the organizational guidelines in this step: Which specialist departments are involved, which roles bear responsibility and who validates the results? It also makes sense to define the time horizons under consideration (short, medium and long term) at this stage, as many sustainability issues have a delayed effect. The approach to stakeholder involvement is also defined in this step, including the question of how the perspective of nature is taken into account, for example via scientific data, site analyses or external studies as a "proxy".

A longlist of potentially relevant topics is compiled on the basis of the scope. The ESRS provide a good structure for this, as they divide the sustainability topics into thematic areas and sub-topics. In practice, however, it is rarely sufficient to simply adopt the ESRS system. Companies should add sector- and company-specific topics to the longlist, especially as long as sector-specific standards are not available or transition periods apply.

Internal analyses alone are often not sufficient for a complete overview of topics. Findings from risk and compliance processes, reports from complaint or whistleblower systems, results from audits and supplier evaluations as well as customer requirements, for example from tenders, are also helpful. External risk indicators can also help, for example on countries, raw materials or locations. This step is not yet about prioritization, but about ensuring that no important issue is overlooked.

Based on the longlist, experts for each topic look at the specific impacts, risks and opportunities for the company (IROs). It is important to note that this does not just happen within the company itself. Many IROs arise along the entire value chain. Particularly in the case of human rights or environmental issues, the greatest impact is often on suppliers (upstream). However, risks and opportunities can also arise later, for example when the product is used, due to customer requirements or during disposal and recycling (downstream).

To avoid misunderstandings later on, the IROs should be clearly categorized during the survey: Impacts as positive or negative and as already occurred or only possible, and risks/opportunities as factors that affect the company from the outside (outside-in). It also helps to record a few basics for each IRO: Where does it occur (own operations, supply chain, use/disposal), who or what is affected, what time period is relevant and what is the assessment based on. Topics for which no comprehensible IROs can be found can then be deleted, because without an IRO, a topic cannot be meaningfully justified in the context of double materiality.

The evaluation shows whether the process is really intended to be "double". This is because impact and financial materiality follow different logics and should therefore be evaluated separately - even if the results can influence each other later on.

In the case of impact materiality, the severity of a negative impact is assessed, for example according to how large it is (extent), how many or which areas are affected (scope) and whether it can be reversed (irreversibility). If a negative impact is only possible, there is also the question of how likely it is. Positive impacts are also considered, especially in terms of how relevant the contribution is. It is important that criteria and scales are clearly defined in advance so that different specialist areas arrive at comparable results.

For financial materiality, an assessment is made as to whether a sustainability issue can influence the financial situation or the business model as a risk or opportunity. The focus here is usually on probability and financial extent, supplemented by time horizons and, if applicable, sensitivities (e.g. dependence on certain raw materials, locations or customer segments). In practice, a comparison with existing risk management is worthwhile, but without reducing the analysis to this: Many sustainability issues are not yet or only incompletely mapped in traditional risk catalogs.

Based on the defined criteria, thresholds are set above which IROs are considered material. Elements that are close to the materiality threshold should be specifically checked for plausibility and, depending on their level of maturity, corroborated with additional data, external sources or expert feedback.

After the assessment, the IROs classified as material are assigned to the respective topics (and sub-topics) and aggregated in a meaningful way. The question of granularity is key here: companies must decide whether they want to report at topic level or differentiate more at sub-topic or IRO level. The ESRS deliberately provide leeway here, but demand traceability.

In practice, it is worth working internally with an IRO register. This clearly documents the main impacts, risks and opportunities, including the assessment logic. A traditional materiality matrix can also be helpful, but often leaves out important details because it only roughly shows the IRO level and the difference between impact and financial materiality. No matter which format you use: In the end, the results should be confirmed by management - as a genuine governance decision, so that the process can also be audited and verified later on.

The real added value arises when the result is consistently transferred to implementation. The next step is to map the key topics and IROs to the relevant ESRS requirements: Which thematic standards are essential, which disclosures and data points are required, and what information needs to be obtained along the value chain?

This is usually followed by a gap analysis. It shows specifically where the company stands: What data is already there, what is still missing, which processes are unclear, where IT support is needed and which controls are required to ensure that the information is standardized and verifiable later on. These results are then used to create a roadmap with responsibilities, a timetable and clear priorities, coordinated with the relevant specialist departments. In this way, the materiality analysis does not stop at reporting, but becomes a tool that sensibly combines sustainability with strategy, governance and risk management.

By consistently applying these steps, companies can not only formally comply with dual materiality, but also use it as it is intended in the logic of the ESRS: as a sound basis for prioritized reporting and at the same time as an orientation for resilient, future-proof corporate management.

Conclusion

Under CSRD and ESRS, dual materiality is more than a formal starting point: it defines which sustainability issues are truly material, from two perspectives. Internal materiality shows the impact on the environment and society, external materiality the financial risks and opportunities for the company.

The added value lies in the implementation: a good materiality analysis not only provides the basis for reporting, but also clear results such as methodology, IRO register, ESRS mapping and a gap analysis. This makes it a management tool that combines sustainability with strategy, governance and risk management.

Frequently asked questions

Double materiality means that companies evaluate sustainability from two perspectives: How ESG issues affect their financial position and what impact their actions have on the environment and society. Due to requirements such as NFRD and CSRD, the concept is becoming increasingly important and helps companies to better integrate responsibility and strategy.

The difference is quickly explained: simple materiality only asks what is financially relevant for the company or investors, i.e. how ESG issues influence profits, risks or company value. Double materiality goes one step further and also looks at what impact the company itself has on the environment and society.

A materiality analysis based on double materiality usually proceeds as follows: First, the objective and scope are defined, then the most important stakeholders are involved. The company then collects possible topics, evaluates them from an impact and financial perspective and prioritizes the key points. The results are documented, incorporated into reporting and regularly updated so that they match the reality of the company.

As a rule, a materiality analysis should be updated every 1 to 3 years and whenever something fundamental changes, for example due to a merger, new products, a new strategy or major external events. It also makes sense to collect feedback from stakeholders on an ongoing basis and incorporate it where necessary. It is best to link the analysis to the annual planning process so that new risks and opportunities can be incorporated directly into decisions.

To ensure that all relevant stakeholders are taken into account, companies should first clarify who they include, for example employees, customers, investors, suppliers or NGOs. Various formats such as surveys, interviews or workshops then help to gather different perspectives. It is important to explain the process transparently, take feedback seriously and, at the end, show what happens as a result - i.e. how the results are incorporated into decisions. You should also consciously include groups that are otherwise easily overlooked.

ESG criteria are important for dual materiality because they cover both sides: they show which sustainability issues can affect the company financially and where the company itself has an impact on the environment and people. At the same time, they help to meet the expectations of investors and other stakeholders, comply with regulatory requirements and identify opportunities for competition and innovation.

Impact materiality looks at what effects a company's actions have on the environment and people, both positive and negative. In contrast to financial materiality, it is not about what affects the figures from the outside, but about what the company itself causes externally and how stakeholders are affected. As expectations and requirements increase, this view is becoming ever more important, also because companies are increasingly required to make their social and ecological effects transparent.

Financial materiality asks which ESG issues are financially relevant for a company, i.e. whether they can influence sales, costs or the company's value. This information is particularly important for investors and must be disclosed depending on the requirements. As part of dual materiality, financial materiality ensures that sustainability issues are not just "nice to have", but are also considered from a risk perspective and for the long-term stability of the company.

Implementing dual materiality is challenging for many companies. There is often a lack of reliable ESG data, stakeholder expectations are not always clear and existing processes need to be adapted, which can also trigger internal resistance. In addition, there are regulatory uncertainties, a lack of expertise and the challenge of measuring non-financial impacts in a meaningful way. And last but not least: The long-term view does not always fit with short-term goals, which makes implementation even more difficult.

Double materiality brings companies clear advantages: they recognize risks and opportunities earlier, financially and in terms of their impact, and can manage them in a more targeted manner. This makes decisions more resilient and helps to build a sustainable strategy that is viable in the long term. At the same time, transparency towards investors, customers and other stakeholders increases, which creates trust and makes it easier to meet regulatory requirements. The bottom line is that this supports stable, sustainable value creation and can trigger innovation.

There are several standards and guidelines that companies can use as orientation for the implementation of dual materiality. SASB is particularly helpful with industry-specific topics, while GRI offers a broad framework for reporting on environmental and social impacts. In the EU, CSRD and ESRS are central because they define the requirements for disclosure. In addition, TCFD (focus on climate-related financial risks) and integrated reporting in accordance with IIRC help to bring together financial and non-financial information.

Dual materiality has a direct impact on corporate strategy. It helps to take a holistic view of risks and opportunities, not only financially, but also in terms of their impact on the environment and people. As a result, companies align their decisions more closely with stakeholder expectations, meet regulatory requirements more easily and strengthen their reputation. At the same time, this can trigger new ideas and innovations and thus support long-term competitive advantages and stable value creation.

Similar mistakes are made time and again in materiality analyses: stakeholders are only half-heartedly involved, the analysis is updated too rarely or the focus is almost exclusively on financial risks, while impact issues are overlooked. There is often a lack of clear objectives, the methodology is unnecessarily complicated and the results are rarely communicated internally. Those who take a structured approach, update regularly and document transparently avoid most of these stumbling blocks.

Larissa Ragg

LinkedInMarketing Managerin · lawcode GmbH

Larissa Ragg verantwortet die Content-Strategie bei lawcode und erstellt Fachbeiträge zu den Themen EUDR, ESG-Compliance, HinSchG, Supply Chain und CSRD. Ihre Beiträge auf dem lawcode Blog machen komplexe regulatorische Anforderungen verständlich und liefern Unternehmen praxisnahe Orientierung.