Important facts

- What is the NFRD?

- The NFRD is an EU directive on non-financial reporting on ESG issues.

- Who is obliged to report?

- Capital market-oriented companies, banks and insurance companies with more than 500 employees Total assets > € 20 million or sales revenue > € 40 million

- What needs to be reported?

- Environmental and social issues, respect for human rights, measures to combat corruption and bribery and diversity concepts in the management bodies must be reported.

- What is the goal?

- More transparency about corporate sustainability and fulfillment of social responsibility.

- Important change

- The NFRD was replaced by the CSRD from 2025 and significantly expanded: more companies, stricter standards, digital reporting obligations.

- Legal framework & control

- The NFRD was transposed into national law in Germany by the CSR Directive Implementation Act, whereby the contents must be published and audited in the management report.

Abstract

The Non-Financial Reporting Directive (NFRD ) is an EU directive from 2014 that obliges large capital market-oriented companies with more than 500 employees to report on non-financial information on ESG aspects. Environmental and social impacts, employee matters, human rights and measures against corruption and bribery must be disclosed.

The reporting obligation increases the transparency and comparability of large companies and strengthens the trust of investors, customers and the public. The reports are published in the management report or in separate sustainability reports and are monitored by the European Commission.

The NFRD laid the foundation for the Corporate Sustainability Reporting Directive (CSRD), which introduces stricter auditing requirements and harmonized reporting standards. Although this means new challenges for companies, it also offers the opportunity to improve sustainability strategies and competitiveness.

Definition and overview

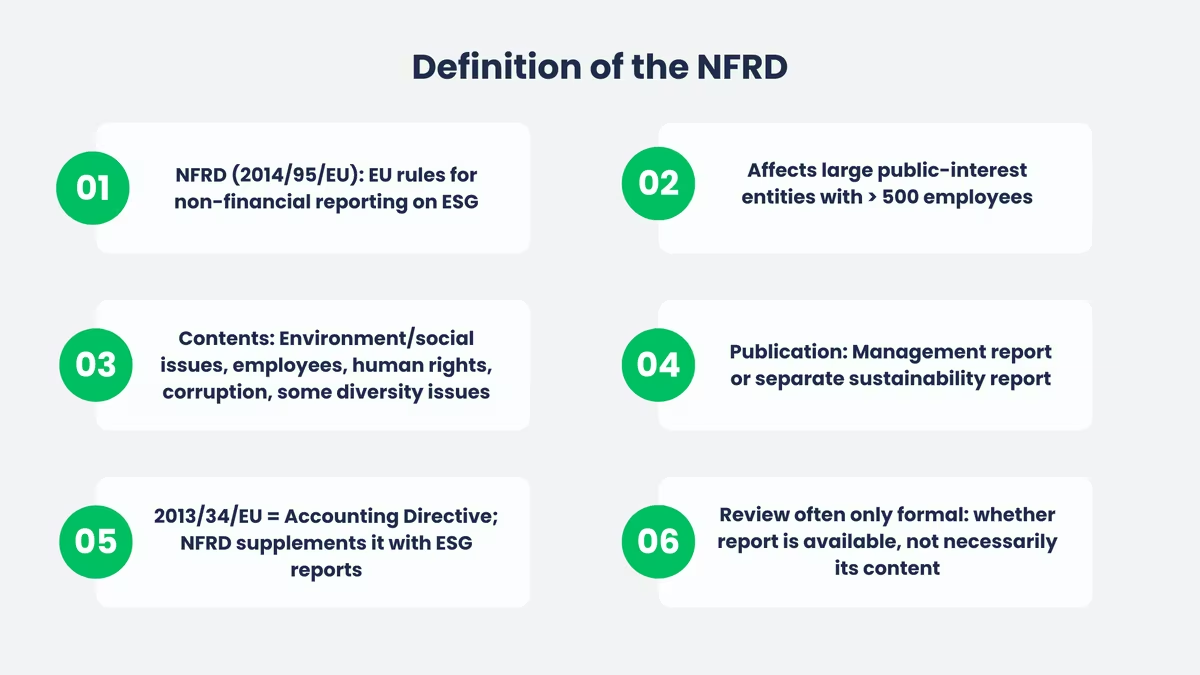

The Non-Financial Reporting Directive (NFRD) is an EU directive that obliges companies to disclose non-financial information. It was introduced in 2014 with the aim of making reporting more transparent, particularly in areas such as the environment, social affairs, corporate governance (ESG) and the fight against corruption and bribery. This should make it easier for stakeholders to understand how responsibly a company is actually acting.

The NFRD (Directive 2014/95/EU) applied to certain large companies and groups that are classified as "public interest entities". If they had an annual average of more than 500 employees, they had to publish a non-financial statement. This included, for example, information on environmental and social issues, employee matters, human rights and the fight against corruption. Directive 2013/34/EU is the Accounting Directive and primarily regulates annual financial statements, consolidated financial statements and management reports. The NFRD (2014/95/EU) builds on this and supplements these requirements with the obligation for non-financial reporting.

The directive required companies to publish this information either in the management report or in a separate sustainability report. In this report, they should explain - particularly with regard to the specification of specific measures - how they deal with issues such as the environment and social issues and what they specifically do to avoid or reduce risks to people and the environment.

An important point of the NFRD was that companies had to disclose how they are positioned with regard to environmental, social and governance (ESG) issues. This was intended to create more trust and at the same time increase the pressure to operate more sustainably. Because the reports were structured according to similar guidelines, companies could also be better compared with each other.

With the directive on non-financial reporting, the EU has taken an important step towards anchoring sustainable business practices more firmly in companies and gearing markets towards a greener future. For some companies, the implementation was initially complex and unfamiliar. However, many also saw it as a real opportunity: Those who report transparently at an early stage and take sustainability seriously can clearly set themselves apart and benefit from this in the long term.

Under the NFRD, in many cases there was no obligation to audit the content as there was under the CSRD. Auditors often had to primarily check whether a non-financial statement or a separate report was provided.

Background to the directive

The idea of disclosing non-financial information emerged in the early 2000s, when there was a growing awareness in the EU that companies not only bear economic responsibility, but also social and environmental responsibility. Global issues such as climate change, social inequality and corporate scandals increased the pressure for more transparency and standardized, comparable sustainability reports.

In 2014, the EU adopted the NFRD, which was implemented in Germany via the CSR Directive Implementation Act (CSR-RUG). Since then, large companies with more than 500 employees have had to report on how they are positioned with regard to environmental, social and governance issues.

The directive pursued two central objectives: To provide investors and stakeholders with a better basis for decision-making and to encourage companies to act more sustainably. Standardized reporting requirements also increase comparability. This is an advantage for companies that want to communicate their sustainability performance clearly.

The NFRD was just the beginning: the Corporate Sustainability Reporting Directive (CSRD) will further tighten the requirements in order to further increase transparency and comparability.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

Comparison: NFRD vs. CSRD

Differences and similarities

The European Union has developed two important directives to promote sustainability in companies: the Non-Financial Reporting Directive (NFRD) and the Corporate Sustainability Reporting Directive (CSRD). Both directives aim to promote transparency and accountability. However, there are significant differences and similarities that need to be considered.

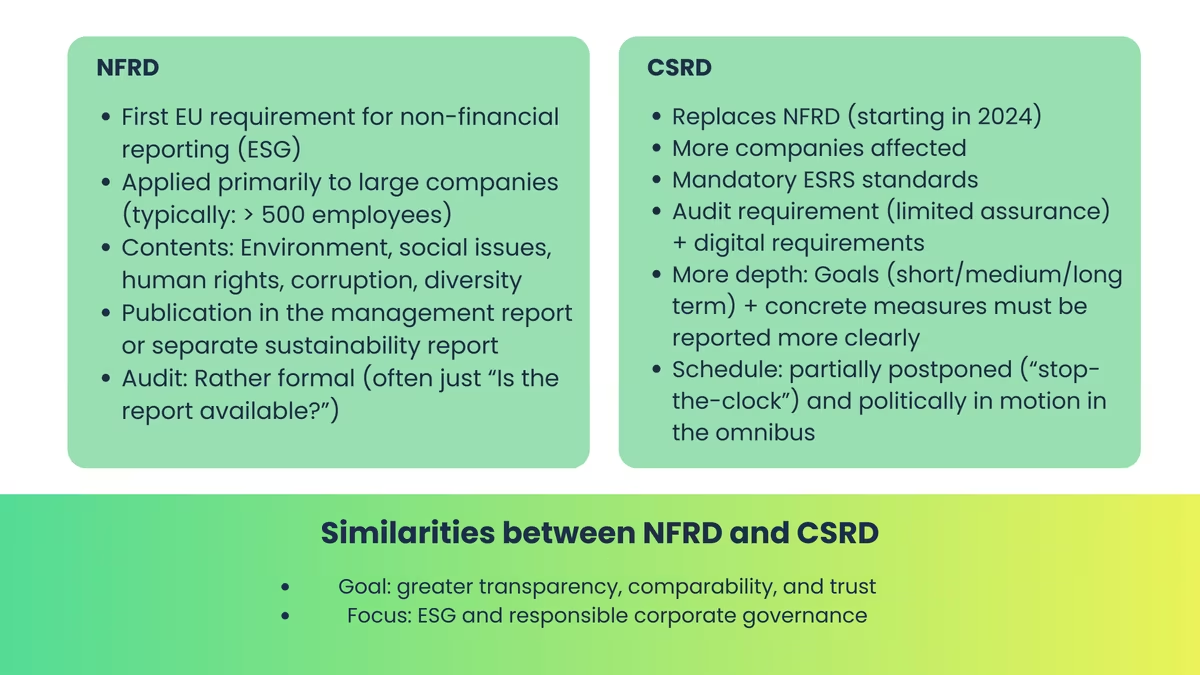

The NFRD was the first EU directive to oblige large companies to report on non-financial information - i.e. on aspects that go beyond pure financial information. The aim was to create uniform standards for the disclosure of environmental, social and governance aspects. Companies with more than 500 employees had to submit reports on their sustainability practices, employee matters, human rights, anti-corruption and diversity. These reports were to be included in the management reports or published as separate sustainability reports.

The CSRD has replaced the NFRD since 2024 and introduces mandatory ESRS standards, auditing and digital requirements. However, the "stop-the-clock" Directive (EU) 2025/794 has postponed the entry dates for many companies by two years. At the same time, the CSRD scope of application is being politically reshaped as part of the omnibus package (provisional agreement Dec 2025). While the NFRD was only applied to large companies, the CSRD(more on the CSRD) now also includes listed small and medium-sized enterprises (SMEs) and other large companies that were previously not covered by the Non-Financial Disclosure Regulation. This leads to a significant expansion of the scope of application.

Another important difference is the scope and depth of reporting. The CSRD requires more detailed and comprehensive disclosures on ESG criteria. Public interest entities must now disclose specific information on their short, medium and long-term sustainability goals and the measures they are taking to achieve these goals. The CSRD also requires reports to be prepared in accordance with uniform European standards and audited by independent third parties.

Both directives aim to improve the transparency and comparability of sustainability reporting and strengthen the confidence of investors and the public. Both the regulation on the disclosure of non-financial information and the CSRD promote more sustainable corporate governance and contribute to a responsible economic system.

Transition from NFRD to CSRD

The change from the NFRD to the CSRD entails more comprehensive and stricter reporting obligations. The most important changes at a glance:

- Expansion of the scope of application: Significantly more companies will be subject to reporting requirements, including those that were not previously subject to the NFRD.

- Stricter audit requirements: In future, information must be verified by independent auditors instead of being based purely on self-declarations, as was previously the case.

- Harmonized reporting standards: Uniform European standards ensure better comparability between companies and sectors.

What does this mean for companies?

The transition is a challenge, but also an opportunity:

✅ Improve sustainability strategies and communicate them more clearly

✅ Strengthen trust among investors, customers and stakeholders

✅ Minimize legal risks through compliant reporting

✅ Achieve competitive advantages through demonstrable sustainability performance

Who is affected by the NFRD?

Company types and criteria

The directive was aimed at large companies that play a significant role in the European economy. But which companies are specifically obliged to report?

It applies to all companies that meet the following criteria:

- Number of employees: Companies with an average of more than 500 employees.

- Balance sheet total: A balance sheet total of more than 20 million euros.

- Turnover: An annual turnover of more than 40 million euros.

Large listed companies, credit institutions and insurance companies in the EU must prepare non-financial reports. The aim is to increase the transparency and accountability of these companies and to strengthen the trust of investors, customers and the public.

These companies must regularly report on how they deal with environmental, social and governance issues. This includes, for example, their environmental impact, social issues, employee and human rights as well as how they deal with corruption and bribery. The purpose behind this is clear: companies should work more sustainably and identify problems in these areas at an early stage and avoid them as far as possible.

An important point is that companies must disclose which sustainability goals they are pursuing. They should explain how they incorporate issues such as the environment, social issues and good corporate governance into their decisions and what they are actually doing to become more sustainable. This makes it easier to compare companies with one another. And that increases the pressure to really act sustainably, not just talk about it.

However, there are also exceptions and special regulations that can limit the scope of the directive on non-financial reporting. Small and medium-sized enterprises (SMEs) are generally exempt from the reporting obligation, unless they are listed on a stock exchange. Subsidiaries whose parent company already submits a consolidated report in accordance with NFRD requirements may also be exempt from the individual reporting obligation.

EU member states can define additional requirements or simplifications to the NFRD. Companies must therefore carefully examine the specific regulations of their member state and ensure that they comply with all national regulations. The Non-Financial Reporting Directive is flexible and adaptable through exemptions. It promotes uniform reporting in the EU. This supports sustainable corporate governance and increases transparency for all stakeholders.

Legal requirements and scope of application

Detailed requirements of the NFRD

The Non-Financial Reporting Directive provides clear guidelines on what non-financial information companies must disclose. This includes reporting on their environmental issues, social impact and corporate governance.

These reports are intended to achieve one thing above all: greater transparency. This enables investors and other stakeholders to better assess how responsibly a company acts and build trust.

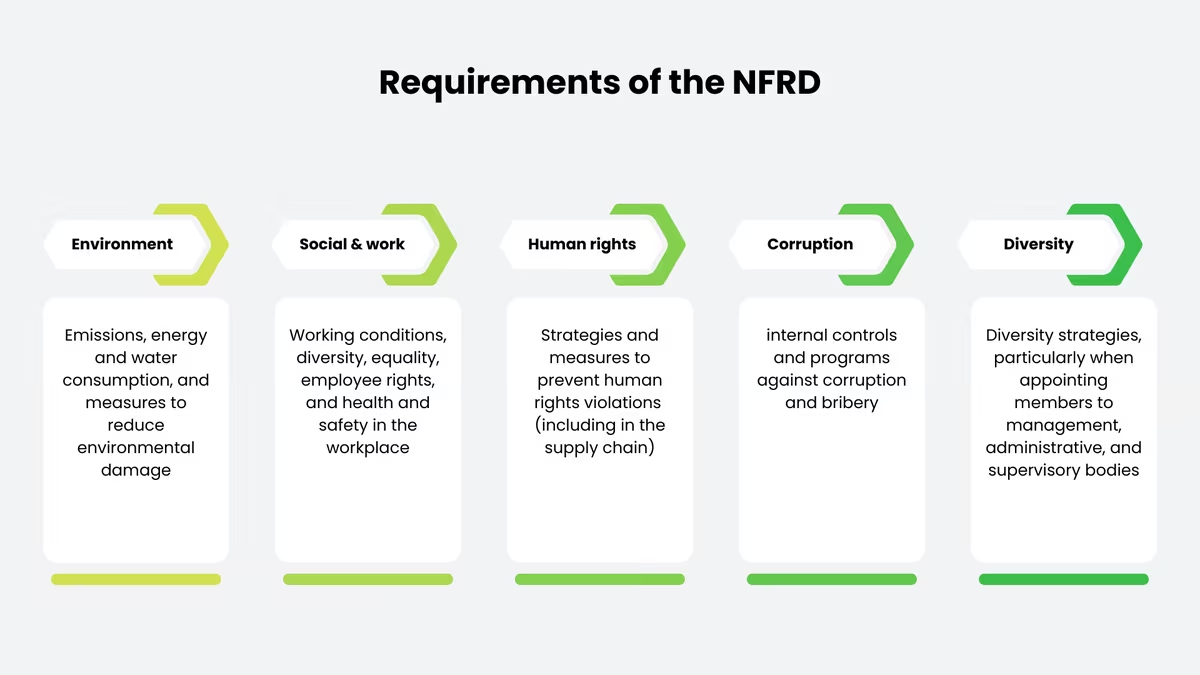

Companies are obliged to disclose information on the following aspects:

- Environmental matters: Information on the current and future impact of the company's activities on the environment, such as greenhouse gas emissions, energy consumption, water consumption and measures to reduce environmental damage.

- Social issues and employee rights: Information on working conditions, measures to promote diversity, equality and compliance with employee rights as well as ensuring health and safety in the workplace.

- Respect for human rights: Disclosure of strategies and measures to prevent human rights violations throughout the supply chain.

- Anti-corruption and bribery prevention: Reporting on internal controls and programs to prevent corruption and bribery.

- Diversity concepts: Presentation of diversity strategies, in particular with regard to the composition of the company's administrative, management and supervisory bodies.

This information must be published in the management reports of the companies or in separate sustainability reports. The reports should be prepared in accordance with recognized reporting standards, such as the guidelines of the Global Reporting Initiative (GRI) or the standards of the Sustainability Accounting Standards Board (SASB). This ensures a high level of comparability and reliability of the information.

Step-by-step guide to the NFRD report

The preparation of an NFRD report starts with thorough planning. First, the company forms a team from various departments, such as Finance, Sustainability, Human Resources and Legal. This team coordinates the entire reporting process and ensures that all relevant information is collected and presented in a structured manner.

A clear plan is needed for implementation to work: who does what and by when? It is also important to know the exact requirements of the NFRD and to decide early on which standard should be used for reporting, for example GRI or SASB.

Many companies seek additional support for this, for example from external consultants or auditors. This helps to comply with legal requirements and create a report that is clean and comprehensible.

The next step is to collect and analyze relevant data. This is often the most time-consuming part, as a lot of different information has to be collected and evaluated. Companies need to collect data on the environment, social aspects, employee rights, human rights and anti-corruption. This data comes from internal sources such as environmental management systems, employee surveys, supplier evaluations and compliance reports.

The data collected must be analyzed in detail in order to identify trends and risks and derive measures to improve sustainability. A thorough analysis helps to identify weaknesses and develop targeted measures to improve ESG performance. The data must be valid and reliable to ensure stakeholder confidence.

The final step is to write and submit the report. It should be clear and structured to maximize readability. A typical structure could include the following elements:

- Introduction: Overview of the company and the objectives of the report.

- Business model: Description of the business model and the most important sustainability factors.

- ESG criteria: Detailed presentation of environmental, social and governance aspects, including specific measures and results.

- Risk management: Information on the identification and management of ESG risks.

- Goals and measures: Presentation of the short, medium and long-term sustainability goals and the steps to achieve them.

- Conclusions and outlook: Summary of key findings and future plans.

Once completed, the report should be reviewed by independent auditors to confirm its accuracy and completeness. The report must then be submitted and published in accordance with legal requirements. This can be done on the company website, in annual reports or in special sustainability reports.

Conclusion

The NFRD has significantly advanced sustainability reporting in the EU. Large companies must disclose how they deal with environmental, social and governance issues, such as human rights, employee concerns and the prevention of corruption. This creates transparency, strengthens investor and public confidence and makes risks and progress more visible and comparable.

At the same time, the reporting obligation brings with it new requirements for data collection and processes, but also offers companies opportunities: those who report credibly and consistently integrate sustainability into their strategy can position themselves positively in the market.

The CSRD is a consistent continuation of this approach: The obligations are being expanded and uniform European standards will make reports even more comparable and meaningful in future. Overall, the NFRD is therefore an important step towards more responsible business practices and long-term corporate success. In future, companies must be prepared to expand their disclosure of non-financial information.

Frequently asked questions

The NFRD is an EU directive (2014/95/EU) that requires certain large companies to disclose non-financial information. The focus is on environmental, social and governance (ESG) issues to make sustainability performance more transparent.

No. Directive 2013/34/EU is the Accounting Directive (annual financial statements, management report, etc.). The NFRD (2014/95/EU) supplements this Accounting Directive with the obligation for non-financial reporting.

This mainly affected "public interest entities" such as capital market-oriented companies, banks and insurance companies. As a rule, the prerequisite was an annual average of more than 500 employees.

In addition to the number of employees, size criteria such as total assets and turnover are often used (e.g. total assets > € 20 million or turnover > € 40 million). The decisive factor in the end is the specific classification according to EU and national law.

Companies had to report on environmental issues, social and employee issues, human rights and anti-corruption, among other things. Diversity concepts in management and supervisory bodies were also included.

The information had to be included in the management report or published as a separate non-financial report/sustainability report. It is important that they are officially accessible and comprehensibly documented.

The NFRD should create transparency so that stakeholders can better assess how responsibly a company is acting. At the same time, it should motivate companies to recognize ESG risks earlier and to operate more sustainably.

Under the NFRD, there was often no review of content as under the CSRD. In many cases, the main focus was on checking whether a non-financial statement or report existed at all.

In Germany, this was implemented via the CSR Directive Implementation Act (CSR-RUG). This transposed the EU requirements into national law and integrated them into the reporting processes.

The CSRD replaces the NFRD and significantly expands the reporting obligations: more companies affected, binding standards (ESRS) and digital requirements. The requirements for auditing and the level of detail of the disclosures are also increasing.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.