Important facts

- What are the ESRS?

- The ESRS (European Sustainability Reporting Standards) are binding European reporting standards for sustainability reporting.

- Who must report in accordance with the ESRS standards?

- All large companies with more than 250 employees, € 40 million in sales or € 20 million in total assets as well as capital market-oriented SMEs.

- What is the aim of the ESRS?

- The standards are intended to ensure uniform, comparable and transparent sustainability reports within the EU.

- How are the ESRS structured?

- There are sector-independent and, in future, sector-specific standards. The most important modules relate to the environment (E), social affairs (S), governance (G) and cross-cutting issues such as strategy, risk management and dual materiality.

- What must be disclosed?

- Companies must provide qualitative and quantitative information on topics such as climate risks, emissions, supply chains, diversity, working conditions and corporate governance.

Abstract

The ESRS are the binding EU standards for sustainability reporting in accordance with CSRD. They provide a standardized framework so that companies can present their sustainability performance in a comprehensible, verifiable and comparable manner between companies, across environmental, social and governance topics.

The initial focus is currently on the sector-independent ESRS (Set 1). Sector-specific standards and standards for certain non-EU companies have been postponed across the EU until June 30, 2026 so that companies can initially focus on Set 1. For companies in the first CSRD wave (reporting year 2024), the EU Commission has also decided on targeted relief ("quick fix") to reduce uncertainty and make it easier to get started.

In terms of content, the ESRS requires reports on impacts, risks and opportunities, so that sustainability becomes visible not only as a collection of key figures, but also as a management and risk issue. In parallel, EFRAG is working on behalf of the EU Commission on proposals to simplify the ESRS in order to reduce the implementation effort without losing the core objectives.

Update (status: February 2026)

The ESRS are now the binding basis for CSRD reporting (ESRS Set 1 applies to financial years from 2024). In addition, certain disclosure requirements and transitional provisions were adjusted via a "quick fix" in order to ease the burden of first-time application. Sector-specific ESRS and standards for certain non-EU companies have been postponed across the EU until 2026. In parallel, EFRAG is working on a simplification or revision of ESRS Set 1 on behalf of the EU. Corresponding technical recommendations were presented at the end of 2025.

Never miss an update on CSRD again.

New specialist articles, regulatory updates and practical tips, straight to your inbox. Once a week, no spam.

What are the European Sustainability Reporting Standards?

The ESRS(European Sustainability Reporting Standards) are the binding European reporting standards according to which companies subject to CSRD must structure their sustainability disclosures. The initial basis is ESRS Set 1 (sector-independent), which applies to financial years from 2024.

The ESRS standards mean something like the sustainability disclosures that should be included in the reports. The aim is reporting that is comparable, auditable and digitally usable and therefore works much better in practice for the capital market, customers, banks and value chains.

The Corporate Sustainability Reporting Directive, or CSRD for short, is a legal framework that obliges companies to produce detailed and reliable reports on their sustainability performance. This link with the European Sustainability Reporting Standards (ESRS) emphasizes the importance of the ESRS for companies. The CSRD requires companies to transparently disclose their environmental, social and governance performance. In doing so, it strategically positions companies in a market that is increasingly environmentally aware. The ESRS and CSRD are part of a comprehensive plan that aims to promote and standardize sustainable practices across the EU economy. This encourages companies to rethink and adapt their sustainability strategies to meet the new requirements.

Impacts, Risks and Opportunities

As the ESRS are part of the EU's Corporate Sustainability Reporting Directive, they set out detailed requirements for companies' sustainability reporting. The terms "impacts", "risks" and "opportunities" play a central role in the context of the ESRS. Here is a brief explanation of what they are all about:

Impacts

"Impacts" refers to the effects that a company has on the environment, society and the economy. This includes both positive and negative effects. As part of the ESRS, companies must explain how their business activities and practices influence the following aspects:

- Environment: emissions, use of resources, waste production, etc.

- Social: working conditions, human rights, communities, etc.

- Economy: Local economy, jobs, added value, etc.

Risks

"Risks" refers to the risks that may arise for the company itself as a result of sustainability aspects. These include

- Physical risks: Risks due to climate change such as extreme weather events, rising sea levels, etc.

- Regulatory risks: Risks from new laws and regulations in the area of sustainability.

- Reputational risks: Risks resulting from public perception and stakeholder expectations.

Opportunities

"Opportunities" refers to the chances that can arise from sustainable business activities. These opportunities may include

- Market opportunities: New markets and customers through sustainable products and services.

- Cost savings: Efficiency gains through sustainable practices and technologies.

- Reputation gains: Strengthening the brand and corporate image through sustainable action.

Implementation in reporting

Companies must report comprehensively on these three aspects as part of the ESRS.

This includes:

→ Identification and assessment: Analysis of material sustainability impacts, risks and opportunities.

→ Measures and strategies: Presentation of the strategies and measures taken to minimize negative impacts, manage risks and exploit opportunities.

→ Targets and progress: Setting specific targets and reporting on progress towards these targets.

By considering "impacts", "risks" and "opportunities", companies should provide a comprehensive picture of their sustainability performance and the associated challenges and opportunities. This not only helps to meet legal requirements, but can also contribute to strengthening stakeholder confidence and long-term success.

Background and development

The development of the European Sustainability Reporting Standards is deeply rooted in the vision ofthe European Green Deal to establish a pioneering role for the EU on the path to a sustainable, inclusive economy that is climate-neutral by 2050. This goal requires major changes in all sectors of the economy. Clear and reliable reporting on sustainability is considered very important in this context.

In this context, the Sustainable Finance Disclosure Regulation, or SFDR for short, provides a legal framework that offers investors clear information on the sustainability risks and opportunities of financial products. The disclosure requirements can be used to channel the flow of capital into more sustainable economic activities. The SFDR shows how environmental, social and governance(ESG) are taken into account in investment decisions and advice. It is therefore important to have standardized, comparable and reliable ESG data.

As a result, it has become clear how important it is to have uniform and comprehensive reporting on environmental, social and corporate governance. This enables various groups, such as investors, customers and politicians, to receive reliable information. To meet this need, the European Financial Reporting Advisory Group (EFRAG) is developing European standards for sustainability reporting. This initiative aims to create a uniform format for measuring, comparing and evaluating the sustainability of EU companies. In November 2022, EFRAG published the first set of ESRS.

The ESRS consider sustainability in all areas - environment, society and corporate governance. They want to improve reporting on these topics so that it is more than just a duty. The aim is to make companies more valuable and strengthen the trust of their stakeholders.

Setting binding sustainability reporting standards for large companies in the EU is an important step forward for Europe's sustainability goals. The ESRS standards provide a clear framework for sustainability reporting. They respond to the desire for greater transparency and at the same time help to accelerate the transition to a more sustainable economy. The European Commission voted on the ESRS on July 31, 2023.

The first mandatory version (ESRS Set 1) was issued by the European Commission as Delegated Regulation (EU) 2023/2772 and applies to financial years from 2024. Targeted quick-fix amendments followed in July 2025 to ease the initial application for companies in the first wave and create more certainty for implementation.

Quick Fix: Reliefs for the first application

The EU has adopted specific transitional and simplification rules ("quick fix") so that companies in the first CSRD wave can prepare their reports in a more practical manner. This mainly concerns selected disclosure requirements and their dates of application. The aim is to reduce complexity in the first reporting year without changing the core of the ESRS.

Core features of the ESRS

The European Sustainability Reporting Standards (ESRS) are an important step forward in environmental, social and governance reporting. They provide companies with a detailed system to make their sustainability practices clearer and more accountable. The key features of the ESRS aim to set a common standard that thoroughly addresses the diverse and complex challenges of sustainability.

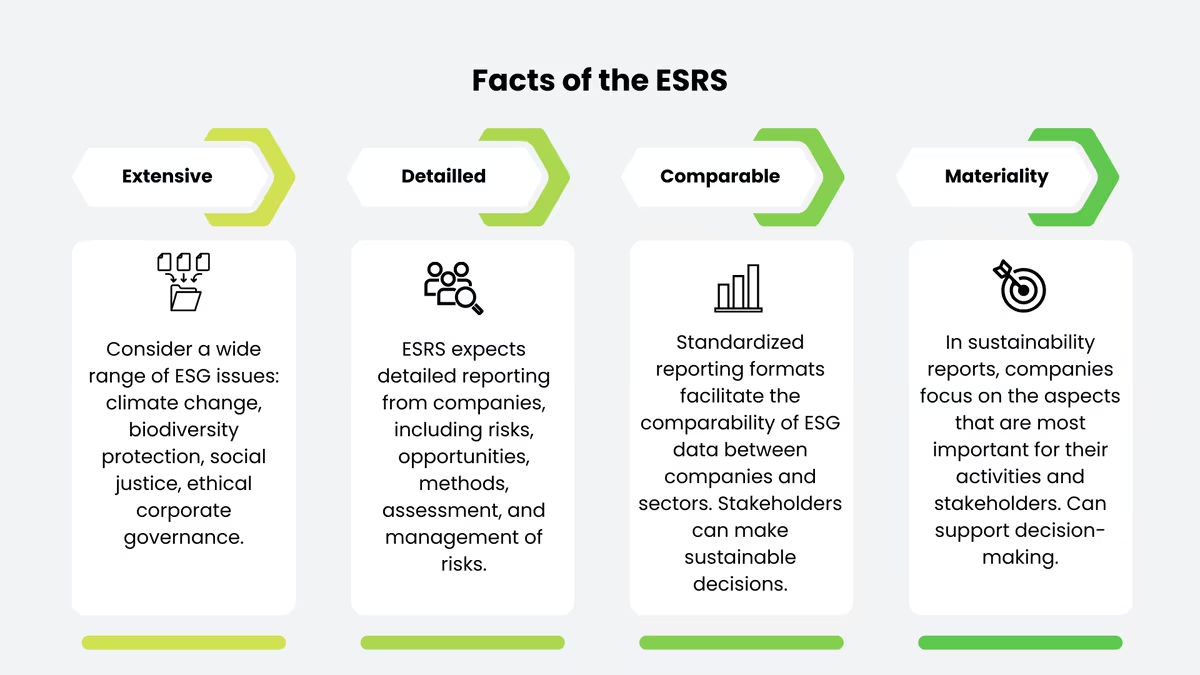

Extensive

The ESRS cover more than usual reports and deal with many important topics for sustainable development. These include areas such as climate change, biodiversity conservation, social justice and ethical business management. By covering a range of topics, the standards ensure that companies present a comprehensive picture of their sustainability and its impact. This makes environmental, social and governance reporting more relevant and effective.

Detailed

Another feature of the EU directives on sustainability reporting is the level of detail required of companies. In addition to ESG measures, companies must also disclose risks and opportunities. This includes methods to identify, assess and manage these risks. More detailed information should help all stakeholders to better understand a company's ESG performance and make informed decisions.

Comparable

By introducing standardized reporting formats and metrics, the ESRS facilitate the direct comparison of ESG data between companies and sectors. This comparability is very important for investors and other stakeholders who want to make sustainable decisions. The ability to compare the sustainability performance of different companies helps to raise awareness of good practice and encourage competition for sustainability.

Focused on materiality

A central principle of the European sustainability reporting standards is the emphasis on materiality, also known as materiality assessment. Companies are encouraged to focus on the sustainability aspects that are most relevant to their specific business activities and stakeholders. This includes the consideration of double materiality, where both environmental impacts and social aspects are relevant. This means that reporting must be tailored and clearly focused to show the particular challenges and opportunities that a company sees in its sustainability efforts. It is important that the reports are not only comprehensive and detailed, but also relevant and targeted to help with decision-making.

The standards in detail

The introduction of the European Sustainability Reporting Standards(to the standards) was initiated by the European Financial Reporting Advisory Group (EFRAG) on behalf of the European Commission. It marks an important milestone in the evolution of sustainability reporting within the European Union.

The new standards are divided into two sets, data points: One for all sectors (Set 1) and one that will be defined later for specific sectors (Set 2). They are intended to enable reporting that addresses the specific needs of different sectors while at the same time respecting the EU's environmental and social objectives.

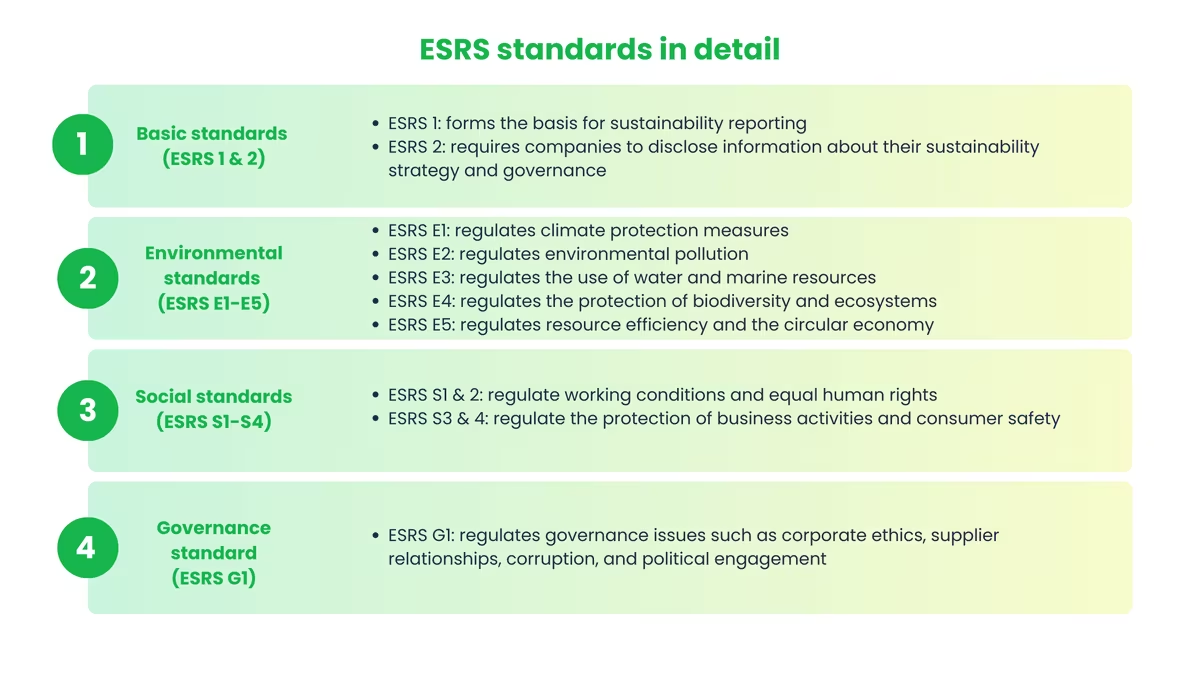

Basic standards ESRS 1 and ESRS 2

- ESRS 1 lays the foundation for sustainability reporting by establishing basic requirements and formal reporting guidelines. This standard is designed to create a consistent starting point for all companies.

- ESRS 2 places higher demands on companies. It requires them to disclose material information about their sustainability strategy and management. This includes an explanation of how companies identify and address sustainability impacts, risks and opportunities, as well as the measures they take to monitor and manage their objectives and performance in these areas.

Environmental standards (ESRS E1 - E5)

These standards address specific environmental issues that are crucial to achieving the EU's environmental goals:

- ESRS E1 focuses on climate change mitigation and adaptation, including reporting on emission reduction strategies.

- ESRS E2 deals with environmental pollution and requires transparency on the release of pollutants.

- ESRS E3 focuses on the management of water and marine resources, calls for reports on water consumption and protective measures for aquatic ecosystems.

- ESRS E4 addresses the protection of biodiversity and ecosystems and expects companies to assess their impact on natural diversity.

- ESRS E5 focuses on resource efficiency and the promotion of a circular economy in order to minimize the ecological footprint.

Social standards (ESRS S1 - S4)

These standards cover a broad spectrum of social responsibility areas:

- ESRS S1 and S2focus on working conditions, equality and human rights within the company and at suppliers.

- ESRS S3 and S4 focus on the protection of communities affected by business activities and the protection and security of consumers and end users.

Governance standard (ESRS G1)

- ESRS G1 addresses topics such as business ethics, relationships with suppliers, corruption and political commitment. It shows how important good corporate governance is in order to promote sustainable development.

The ESRS standards provide a clear framework for companies to openly and consistently demonstrate and improve their sustainability. This helps to increase awareness and responsibility for environmental and social issues.

Advantages and disadvantages for companies

The new European standards for sustainability reporting are an important step for companies. They bring both advantages and challenges. This detailed examination of the advantages and disadvantages shows what companies need to pay attention to when reporting.

Advantages for companies

Improved transparency and credibility with investors and customers:

When companies report in accordance with European standards, they show that sustainability is important to them. This makes them more trustworthy and improves their reputation with current and future investors and customers. This openness can attract more customers and interest investors who value sustainability.

Easier identification & management of ESG risks and opportunities:

The detailed reporting requirements of the ESRS enable companies to analyze their ESG risks and opportunities in greater depth. This leads to companies understanding their sustainability better. They can then act more quickly to reduce risks and take advantage of opportunities. This approach can make the company stronger and more competitive.

Strengthening sustainable financing options:

If companies comply with European sustainability reporting standards, their access to environmentally friendly financing improves. Many investors and banks want to see clear evidence that a company is acting sustainably. This can lead to better credit conditions and help companies to finance their environmental goals.

Disadvantages for companies

High implementation and reporting costs:

Adapting to the detailed reporting requirements of the new European standards can be expensive. A lot may need to be invested in new systems, processes and training. This could be particularly difficult for smaller companies because they often do not have as many resources as large companies.

Complexity of requirements can be a challenge:

The complexity and scope of reporting can be difficult for companies of all sizes. It is necessary to address many different ESG (environmental, social, governance) issues and provide accurate information. This requires good planning and perhaps new systems for managing and analyzing data.

The new European sustainability standards bring challenges for companies, such as high start-up costs and difficult implementation. But they also provide an opportunity to become more open and trustworthy when it comes to sustainability. By teaching companies to better manage environmental, social and corporate risks and to utilize new sources of financing, these standards can help them to be more stable and successful in the long run.

It is a good idea to see the application of the new European sustainability reporting standards as an investment in the future. They not only help you to comply with the law, but also promote sustainability and the value of your company.

Practical steps to prepare for the ESRS

To prepare for the new European sustainability reporting standards, companies should plan well and strategically. Careful planning will help to follow the new rules and use them as an opportunity to improve sustainability and report on it more openly. Here are some useful steps to take:

Practical steps for implementation

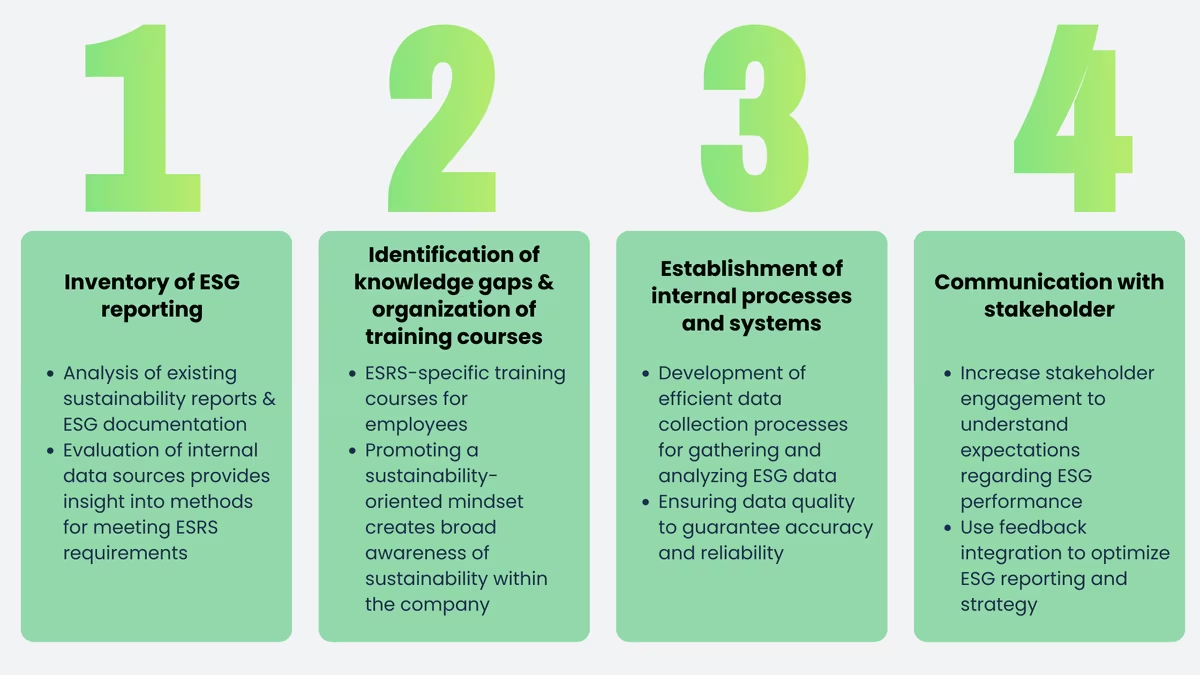

- Analyze existing reports: Start by closely reviewing your current sustainability reports and ESG documents. Compare these with the new EU standards to find out what has already been implemented correctly and what is still missing.

- Evaluate internal data sources: Look at what internal data sources you already use and how you collect, store and process this data. This will help you understand whether your current systems are good enough or whether you need to change them to comply with the new EU standards.

- ESRS-specific training: Organize training for your employees who work on reporting so that they understand the new EU standards and how they differ from previous methods.

- Promote a sustainability-oriented mindset: Expand your training programs to raise awareness of sustainability throughout the company. This supports a corporate culture in which sustainability is anchored in all business areas.

- Develop efficient data collection processes: Implement processes that allow you to systematically collect and analyze environmental, social and governance (ESG) data. This may require the use of specialized sustainability management software.

- Ensuring data quality: Establish rules and processes to ensure the quality of your data. This includes regular checks and confirmations to ensure that the information you report is accurate and reliable.

- Stakeholder engagement: Create a plan to engage with your stakeholders so that you understand their expectations of your sustainability performance and reporting. This could include workshops, surveys or regular meetings.

- Feedback integration: Use feedback from stakeholders to improve your sustainability plans and reports. Talking openly about your successes and problems builds trust and credibility with all stakeholders.

If your company is not subject to CSRD but needs to respond to data requests from the value chain, the VSME standard provides a pragmatic, EU-recommended framework for structured ESG information.

Preparing for the EU guidelines on sustainability reporting and thus for the ESRS is complicated, but it is worth it. It not only helps companies to comply with rules, but also to become more sustainable. If companies involve all parts of their organization and focus more on sustainability, they can not only improve their reports according to the European standards. They can also be good for the environment and society in the long term.

Conclusion

The introduction of the ESRS is an important step towards greater transparency and comparability in sustainability reporting in the EU. Standardized requirements make ESG data more reliable and help companies to integrate sustainability more strongly into their strategy, management and processes - not just as an obligation, but as an opportunity for long-term resilience and competitiveness.

In this way, the ESRS support key EU goals, such as climate neutrality and a more socially just economy. At the same time, they can help to channel capital flows more strongly into sustainable technologies and projects, as investors and stakeholders can make more informed decisions.

Parallel to implementation, the requirements are being made more practicable: EFRAG is working on simplifications for ESRS Set 1 on behalf of the EU Commission, and sector-specific standards have been postponed across the EU until 2026 so that companies can initially focus on the sector-independent principles.

Frequently asked questions

The European Sustainability Reporting Standards are standards set by the EU Commission that require companies to disclose detailed information about their sustainability practices. They cover a wide range of topics, including environmental, social and governance issues, and aim to improve the transparency and comparability of sustainability reporting in the EU. The ESRS were developed by the European Financial Reporting Advisory Group (EFRAG) and are a central component of the Corporate Sustainability Reporting Directive.

Large companies that meet at least two of the following criteria are affected: a balance sheet total of EUR 25 million or more, net sales of EUR 50 million or more and a workforce of 250 or more. Listed small and medium-sized enterprises (SMEs) with more than 10 employees, excluding micro-enterprises, are also subject to this obligation. The introduction will be gradual: From 2024 for companies already subject to reporting requirements, from 2025 for all large companies and from 2026 for listed SMEs.

The European Sustainability Reporting Standards require companies to identify and assess their impacts, risks and opportunities (IROs) as part of the dual materiality analysis. This involves considering both the company's impact on the environment and society and the impact of sustainability issues on the company itself. This approach makes it possible to identify relevant sustainability issues and develop appropriate measures to minimize risks and exploit opportunities. The IROs therefore form the basis for transparent and comprehensive sustainability reporting in accordance with the standards.

The European Financial Reporting Advisory Group (EFRAG) plays a central role in the development and updating of the ESRS. As technical advisor to the European Commission, EFRAG is responsible for developing and updating the standards. EFRAG develops the ESRS in a transparent process that includes public consultations and the involvement of various interest groups. This ensures that the standards are practical and effective. EFRAG also supports companies during implementation by providing guidelines and explanatory documents to facilitate the application of the standards.

The European Sustainability Reporting Standards are an integral part of the CSRD and define the requirements for sustainability reporting by companies. Companies must disclose detailed information on their material impacts, risks and opportunities in relation to environmental, social and governance issues. Reporting is based on the principle of dual materiality, which takes into account both the company's impact on sustainability issues and the impact of these issues on the company. They comprise general standards (ESRS 1 and ESRS 2) as well as topic-specific standards, each of which contains specific disclosure requirements. Implementation requires companies to carefully analyze their business activities and relationships in order to identify and transparently report relevant sustainability information.

They provide a comprehensive framework for sustainability reporting by covering a wide range of environmental, social and governance (ESG) topics. Companies must take dual materiality into account, i.e. assess both the impact of their business activities on the environment and society and the relevance of sustainability issues for their own business development. Application is mandatory for all companies covered by the CSRD and thus ensures uniform and comparable reporting within the EU. Through standardized disclosure requirements, they promote transparency and comparability of sustainability information, which enables investors and other stakeholders to make informed decisions. In addition, reporting in accordance with ESRS is an integral part of the management report, which means that sustainability aspects are more closely integrated into overall corporate reporting.

The two basic standards include:

- ESRS 1 - General requirements: This standard sets out the principles and concepts for the preparation of sustainability reports, including the principle of double materiality, consideration of the entire value chain and requirements for the presentation of sustainability information.

- ESRS 2 - General Disclosures: This standard defines specific disclosure requirements that apply to all companies, regardless of their industry or size. ESRS 2 includes information on governance structures, strategies, the management of impacts, risks and opportunities as well as objectives and performance indicators.

Together, they form the foundation for uniform and transparent reporting in Europe.

The environment-related standards (E1-E5) are intended to support companies in disclosing their environmental practices. These include the ESRS E1 standard, which focuses on climate change, as well as other standards covering topics such as pollution, water and marine resources, biodiversity and ecosystems, resource use and the circular economy. These standards aim to improve the transparency and comparability of reporting in the EU.

The social standards that require companies to report on their social impacts and responsibilities are divided into S1-S4. These include S1, which focuses on the company's own workforce, S2, which addresses the workforce in the value chain, S3, which considers affected communities, and S4, which focuses on consumers and end users. These standards aim to create transparency about working conditions, human rights and social impacts along the entire value chain.

Governance Standard G1 - Corporate Governance requires companies to disclose information about their management. This includes aspects such as the role of the administrative, management and supervisory bodies, internal control systems, risk management processes and measures to combat corruption and bribery. The aim is to create transparency about corporate governance and strengthen stakeholder confidence.

The standards are developed and regularly updated by the European Financial Reporting Advisory Group. This process includes the preparation of draft standards, public consultations to obtain feedback and the subsequent finalization of the standards. After revision by EFRAG, the standards are adopted and published by the European Commission as delegated acts. Through continuous monitoring and adaptation, EFRAG ensures that the standards always meet the current reporting requirements in the EU.

The application of the standards offers companies several advantages. Standardized reporting in accordance with ESRS enables companies to increase the comprehensibility, relevance and comparability of their sustainability information, which strengthens the trust of investors and stakeholders. They also fulfill the legal requirements of the Corporate Sustainability Reporting Directive and avoid legal risks. Transparent disclosure of sustainable practices can improve access to sustainable financing and serve as a strategic competitive advantage by positively influencing the company's image and strengthening its market position. In addition, ESRS-compliant reporting helps companies to systematically manage their efforts, identify areas for improvement and set meaningful targets, leading to more sustainable business performance in the long term.

Implementation poses several challenges for companies. The collection and integration of extensive data along the entire value chain requires resources and can be difficult due to the complexity of supply chains. In addition, companies must adapt their internal processes in order to comply with the detailed reporting obligations, which can be a considerable burden, especially for small and medium-sized enterprises (SMEs). Alignment with existing international standards such as GRI, SASB or TCFD requires additional efforts to ensure consistency and comparability. Furthermore, ensuring data quality and accuracy, especially when collecting environmental and social data, can be complex and time-consuming. Finally, companies must ensure that they have the necessary internal skills and systems in place to effectively implement the new requirements and ensure compliance.

EFRAG has published several guidelines to support companies with implementation. These include the materiality analysis guide, which explains the process of dual materiality, and the value chain guide, which describes reporting requirements for the entire value chain. In addition, the list of ESRS data points provides a detailed overview of the necessary disclosure requirements. These tools are designed to help companies implement the ESRS efficiently and effectively.

The ESRS are closely linked to other EU sustainability initiatives and serve as a central instrument for implementing the CSRD. They harmonize reporting on environmental, social and governance aspects and support the objectives of the European Green Deal and the EU Taxonomy Regulation by promoting transparency and comparability of sustainability information. By standardizing disclosure requirements, the ESRS make it easier for companies to meet regulatory requirements and help channel capital into sustainable investments.

Karim Boukaouche

LinkedInESG compliance expert - lawcode GmbH

Karim Boukaouche advises companies on the implementation of the EU Deforestation Regulation (EUDR) and supports the implementation of digital solutions for legally compliant supply chains. His specialist articles on the lawcode blog combine regulatory depth with practical recommendations for action.